第11章 时间序列模型

11.1 理论知识

平稳时间序列分析: 平稳的,非随机序列(非白噪声序列)

11.1.1 差分

一阶差分: \(\triangledown{x_t}=x_{t}-x_{t-1}\)

二阶差分: \(\triangledown^2{x_t}=\triangledown{x_t}-\triangledown{x_{t-1}}\) 一阶差分的差分

三阶差分: \(\triangledown^p{x_t}=\triangledown^{p-1}{x_t}-\triangledown^{p-1}{x_{t-1}}\)必须先计算前一阶的差分

k步差分:\(\triangledown_k{x_t}=x_t-x_{t-k}\) 直接相隔k步计算差

11.1.2 延迟算子

当前序列值乘上一个延迟算子,相当于把当前序列值的序列时间向过去拨了一个时刻

记B为延迟算子

\[x_{t-1}=Bx_t\]

\[x_{t-2}=Bx_{t-2}\]

- 用延迟算子表示差分运算

\[\triangledown^p{x_t}=(1-B)^px_t=\sum^p_{i=0}(-1)^pC^i_px_{t-i}\]

\[\triangledown_kx_t=x_t-x_{t-k}=(1-B^k)x_t\]

11.1.3 平稳时间序列

h(t)=

AR(p):p阶自回归模型

\(x_t=\phi_0+\phi_1x_{t-1}+\phi_2x_{t-2}+\dots+\phi_px_{t-p}+\epsilon_t\)

\(\phi_p\neq0\)

-

严宽平稳的联系和区别:

- 严平稳:时间序列的任意n个时刻的联合分布保持不变,即序列的所有统计性质都不会因为时间的推移而发生变化

- 宽平稳:时间序列任意时刻的均值保持不变,二阶矩存在且二阶矩只与时间有关

- 严平稳和宽平稳的关系:

- 如果二阶矩存在,严平稳一定是宽平稳

- 如果是正态分布,则宽平稳代表严平稳

- 如果二阶矩存在,严平稳一定是宽平稳

平稳性的意义

如果序列不平稳,那么序列就会有很多个随机变量,并且每个变量都只有一个样本,通常是没有办法进行分析的。 但是如果序列平稳,那么均值为常数,这样意味着含有可列多个随机变量的均值序列变成了一个常数序列,这样样本数也就变成了时间序列的个数, 这样减少了随机变量数,增加了待估参数的样本容量,降低了时序分析的难度,提高了对均值函数的估计精度

-

平稳时间序列的统计性质

- 常数均值:\(E(X_t)=\mu\)

- 自协方差函数:\(\gamma(t-s)=\gamma(t,s)=E[(X_t-\mu_t)(X_s-\mu_s)]\)

- 自相关函数:\(\rho(t,s)=\frac{\gamma(t,s)}{\sqrt{D(X_t)}\sqrt{D(X_s)}}\)

- 延迟k自协方差函数:\(\gamma(k)=\gamma(t,t+k)\)

- 方差:\(D(X_t)=\gamma(0)\)为常数

- 延迟k自相关系数:\(\rho(k)=\frac{\gamma(t,t+k)}{\sqrt{\gamma(0)}\sqrt{\gamma(0)}}\space=\space\frac{\gamma(k)}{\gamma(0)}\)

11.1.3.1 Wold分解定理

-

Wold分解定理

对于任意一个离散平稳时间序列,都可以分解成两个不相关的平稳序列之和,其中一个为确定性的,另一个为随机性的

\(x_t=V_t+\xi_t\)

\(V_t=\sum_{j=1}^{\infty}\phi_jx_{t-j}\),等价表达为历史序列值的线性函数

\(\xi_t=\sum_{j=0}^{\infty}\theta_j\epsilon_{t-j}\),代表了不能有历史信息表达的部分,其中\(\theta_0=1,\sum_{j=0}^{\infty}\theta_j^2 \leq \infty,\epsilon独立,通常假定0均值正态分布\)

对任意平稳时间序列而言,做线性回归\(y_t=a_0+a_1y_{t-1}+a_2y_{t-2}+\dots+a_py_{t-p}+v_t\)

前面的是确定性部分,后面的\(v_t\)是非确定性部分,它的方差决定了p期历史信息对未来的预测精度

如果方差极限趋向0,则\(y_t\)为确定性序列 如果方差极限趋向\(var(y_t)\),则\(y_t\)为纯随机性序列

绝大多数序列结语确定性序列和纯随机性序列中间,即\(0和var(y_t)\)之间,序列中既包含部分确定性信息,又包含部分随机信息,这是我们把序列简称为随机序列

11.1.3.2 平稳序列的特征根

p阶线性差分方程:\(x_t+a_1x_{t-1}+\dots+a_px_{t-p}=h_t\)

一阶: \[x_t-0.8x_{t-1}=0\] \[\lambda^1-0.8\times \lambda^0=0,得\lambda=0.8\] \[1-0.8B=0,得B=1/0.8\]方程的根是特征根的倒数

二阶: \[x_t-0.6x_{t-1}+0.05x_{t-2}=0\] \[\lambda^2-0.6\lambda+0.05=0,得\lambda_1=0.5,\lambda_2=0.1\] \[1-0.6B+0.05B^2=0 得B_1=2,B_2=10\]

11.1.3.3 平稳序列特征根的性质

平稳序列必须满足特征根的绝对值都小于1

*平稳性检验

- 图检验

- DF检验:当\(\tau\)值小于\(\tau_\alpha时\),拒绝原假设,序列平稳,即序列无单位根,即p值较小时。只能检验最高延迟一阶信息

- 无漂移项自回归结构:\(x_t=\phi_1x_{t-1}+\xi_t\)

- 有漂移项自回归结构:\(x_t=\phi_0+\phi_1x_{t-1}+\xi_t\)

- 带趋势回归结构:\(x_t=\alpha+\beta t+\phi_1x_{t-1}+\xi_t\)

- ADF检验:可以检验更高的延迟阶数

- 只要有一个单位根,则不平稳

- 纯随机性检验

如果序列值彼此之间没有任何相关性,那就意味着该序列是一个没有记忆的序列,过去的行为对将来的发展没有任何影响,这种序列称为纯随机序列,从统计分析的角度,纯随机序列是没有任何分析价值。

- 纯随机序列(白噪声序列)定义:简记为\(X_t\sim WN(\mu,\sigma^2)\)

- 任取\(t\in T,有EX_t=\mu\)

- 任取\(t,s\in T\),有 \[\gamma(t,s)=\begin{cases}\sigma^2 & t=s\\0 & t\neq s\end{cases}\]

- 纯随机序列性质

- 纯随机性

- 方差齐性:序列中每个随机变量的方差相等,如果不满足,则是异方差

- 纯随机性检验

- 如果一个时间序列是纯随机的,得到一个观察期数为n的观察序列,那么该序列的延迟非零期的样本自相关系数将近似服从均值为零,方差为序列观察期数倒数的正态分布,即: \[ \hat{\rho_k} \sim N(0,\frac{1}{n}),\forall k \neq0\]

- 原假设:延迟期数小于或等于m期的序列值之间相互独立

- 备则假设:延迟期数小于或等于m期的序列值之间有相关性

- Q统计量 \[Q_{BP}=n\sum_{k=1}^m\hat{\rho_k}^2\] \[Q_{LB}=n(n+2)\sum_{k=1}^{m}(\frac{\hat{\rho_k}^2}{n-k})\] n为观察期数,m为延迟阶数 这两种Q统计量都服从\(Q\sim \chi^2(m)\)

- 平稳序列的短期相关性,所以一般只需要检验前几期。另一方面,如果一个平稳序列显示出显著的短期相关性,那么该序列就一定不是白噪声序列

11.1.4 AR模型

- 函数形式 \[X_t=\phi_1X_{t-1}+\phi_2X_{t-2}+\dots+\phi_pX_{t-p}+\epsilon_t,或\Phi(B)X_t=\epsilon_t\]

- 统计性质

- 均值\(E(X_t)=\mu\)

- 方差:

- AR(1):\(G_0=1,G_1=\phi_1G_0,G_2=\phi_1G_1,方差\gamma_0=\frac{\sigma_\epsilon^2}{1-\phi_1^2}\)

- AR(2) : \(G_0=1.G_1=\phi_1G_0,G_2=\Phi_1G_1+\phi_2G_0,方差\gamma_0=\frac{1-\phi_2}{(1+\phi_2)(1+\phi_1-\phi_2)(1-\phi_1-\phi_2)}\sigma_\epsilon^2\) \[D(X_t)=\sum_0^\infty G_i^2\sigma_\epsilon^2\]

- 自协方差

- 公式:\(\gamma_k=\phi_1\gamma_{k-1}+\phi_2\gamma_{k-2}\)

- AR(1):\(\gamma_0=D(X),\gamma_1=\phi_1\gamma_0,\gamma_2=\phi_1\gamma_1\)

- AR(2):\(\gamma_0=D(X),\gamma_1=\phi_1\gamma_0+\phi_2\gamma_1得\gamma_1=\frac{\phi_1}{1-\phi_2}\gamma_0\)

- 自相关

- 自协方差函数除以\(\gamma_0\)

- 偏自相关

- yule-Walker方程:写自相关函数的方程

- AR(1):\(\phi_{11}=\phi_1,其他为0\)

- AR(2):\(\phi_{11}=\rho_1=\frac{\phi_1}{1-\phi_2},\phi_{22}=\phi_2,其他为0\)

11.1.5 MA模型

- 均值:\(E(X_t)=\mu\)

- 方差: \(D(X_t)=(1+\theta_0+\dots+\theta_q)\sigma_\epsilon^2\)

- 协方差

- MA(1)\(\begin{cases}(1+\theta_1^2+\dots+\theta_q^2)\sigma_\epsilon^2& q = 0\\-\theta_1\sigma_\epsilon^2 & q = 1\end{cases}\)

- MA(2)\(\begin{cases}(1+\theta_1^2+\dots+\theta_q^2)\sigma_\epsilon^2& q = 0\\(-\theta_1+\theta_1\theta_2)\sigma_\epsilon^2 & q = 1\\ -\theta_2\sigma_\epsilon^2&q=2\end{cases}\)

- 自相关

- 除以方差

- 偏自相关

- yule-walker方程

- MA(1)\(\begin{cases}\phi_{11}=\rho_1=\frac{-\theta_1}{1+\theta_1^2}& k = 1\\ \phi_{22}=\frac{\theta_1^2}{1+\theta_1^2+\theta_1^4} & k= 2\\ \phi_{33}=\frac{-\theta_1^3}{1+\theta_1^2+\theta_1^4+\theta_1^6}&k=3\end{cases}\)

11.1.6 ARMA模型

均值

-

方差:

- 格林公式:\(\begin{cases}G_0=1 & j = 0\\G_k=\sum_{j=1}^k\phi_j^\prime G_{k-j}-\theta_k^\prime & j > 0\end{cases}\)

- ARMA(2,2):\(G_0=1,G_1=\phi_1G_0-\theta_1,G_2=\phi_1G_1+\phi_2G_0-\theta_2,G_3=\phi_1G_2+\phi_2G_1\)

-

自协方差

- \(y_k=\sigma_\epsilon^2\sum_{i=0}^\infty G_iG_{i+k}\)

-

自相关

- \(\rho_k=\frac{\gamma_k}{\gamma_0}=\frac{\sum_{j=0}^\infty G_jG_{j+k}}{\sum_{j=0}^{\infty}G_j^2}\)

ARMA(1,1) \[G_0=1,G_k=(\phi_1-\theta_1)\phi_1^{k-1}\] \[\gamma_0=\frac{1+\theta_1^2-2\theta_1\phi_1}{1-\phi_1^2}\sigma_\epsilon^2\] \[\gamma_1=\frac{(\phi_1-\theta)(1-\theta_1\phi_1)}{1-\phi_1^2}\sigma_\epsilon^2\] \[\gamma_2=\phi_1\gamma_1\] \[\rho_1=\frac{(\phi_1-\theta_1)(1-\theta_1\phi_1)}{1+\theta_1^2-2*\theta_1\phi_1}\] \[\rho_2=\phi_1\rho_1\]

-

偏自相关

- yule-walker方程

11.1.7 Crammer分解定理

任何一个时间序列\({x_t}\)都可以视为两部分的叠加,其中,一部分是由时间t的多项式决定的确定性成分,另一部分是由白噪声序列决定的随机性成分,即 \(x_t=\mu_t+\epsilon_t=\sum_{j=0}^d\beta_jt^j+\Psi(B)a_t\)

Crammer分解定理说明任何一个序列的波动都可以视为同时受到确定性影响和随机性影响的作用,平稳序列要求这两方面的影响都是稳定的,而非平稳的产生的激励就在于它所受到的这两方面的影响至少有一方面是不稳定的

11.1.8 ARIMA模型

\(\Phi(B)\triangledown^dx_t=\Theta(B)\epsilon_t\)

广义自回归多项式:\(\phi(B)=\Phi(B)\triangledown^d\)

ARIMA(p,d,q)模型不平稳,并且序列方差不满足方差齐性

\(x_t=\epsilon_t+\Psi_1\epsilon_{t-1}+\Psi_2\epsilon_{t-2}-\dots\)

广义自相关函数\(\Phi^*(B)=\Phi(B)(1-B)^d=1-\tilde{\phi_1}B-\tilde{\phi_2}B^2-\dots\)

\(\Psi_1=\tilde{\phi_1}-\theta_1\)

\(\Psi_2=\tilde{\phi_1}\Psi_1+\tilde{\phi_2}-\theta_2\)

疏系数模型: \(ARIMA((p_1,p_2),d,q)\)

11.2 实践操作

import pandas as pd

import numpy as np

import statsmodels.api as sm

import statsmodels.tsa.api as tsa

import statsmodels.formula.api as smf

import matplotlib.pyplot as plt

import statsmodels

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.graphics.api import qqplot

from scipy import statsimport warnings

warnings.filterwarnings("ignore")

from IPython.core.interactiveshell import InteractiveShell

InteractiveShell.ast_node_interactivity = 'all'# 导入数据

data=pd.read_excel('../习题与案例数据/案例数据/A1_7.xlsx',index_col='year')

data.index=pd.date_range('1900','1999',freq='a')#不要以年份做索引,可能会有问题

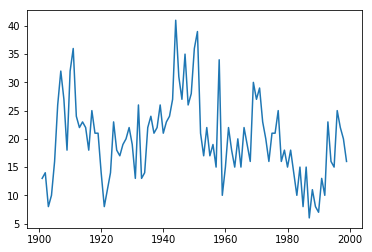

data

11.2.2 模型识别

11.2.2.1 序列的描述性统计

- 序列的平稳性检验结果

adf检验

(-3.183192251191782,

0.02097842525600371,

2,

96,

{'1%': -3.5003788874873405,

'5%': -2.8921519665075235,

'10%': -2.5830997960069446},

549.0681467660734)

maxlag:最大滞后阶数,也就是自回归阶数

regression:自回归项是一定被包括的,maxlag设定了阶数

'c':只有常数项(漂移项)

'ct':漂移项和趋势项

'nc':只有自回归项

'ctt':constant, and linear and quadratic trend

autolag:自动选择lag,基于bic,aic等准则,只有设置为None,自己设置的maxlag才会被使用,否则模型会自动选择最好的lag

其他的见上面返回adf,p值,回归阶数,样本数,0.01,0.05,0.1分位点的值,aic等信息准则的值,等。

(-3.9178563779331284,

0.001907294129421782,

1,

97,

{'1%': -3.4996365338407074,

'5%': -2.8918307730370025,

'10%': -2.5829283377617176})reg=['nc','c','ct']

lag=[0,1,2]

model=['自回归','漂移项+自回归','漂移项+趋势项+自回归']

results=[]

for i in reg:

for j in lag:

types=model[reg.index(i)]

stat,p=tsa.adfuller(data.number,autolag=None,maxlag=j,regression=i)[:2]

results.append([types,j,stat,p])

pd.DataFrame(results,columns=['type','lag','统计量值','p值'])| type | lag | 统计量值 | p值 | |

|---|---|---|---|---|

| 0 | 自回归 | 0 | -1.584539 | 0.106501 |

| 1 | 自回归 | 1 | -1.045064 | 0.266416 |

| 2 | 自回归 | 2 | -0.652610 | 0.432560 |

| 3 | 漂移项+自回归 | 0 | -5.353999 | 0.000004 |

| 4 | 漂移项+自回归 | 1 | -3.917856 | 0.001907 |

| 5 | 漂移项+自回归 | 2 | -3.183192 | 0.020978 |

| 6 | 漂移项+趋势项+自回归 | 0 | -5.551394 | 0.000018 |

| 7 | 漂移项+趋势项+自回归 | 1 | -4.141835 | 0.005471 |

| 8 | 漂移项+趋势项+自回归 | 2 | -3.509947 | 0.038338 |

dir(tsa.adfuller(data.number,regresults=True)[-1])[:2]+dir(tsa.adfuller(data.number,regresults=True)[-1])[-8:]

tsa.adfuller(data.number,regresults=True)[-1].adfstat#返回adf值['H0',

'HA',

'adfstat',

'autolag_results',

'critvalues',

'icbest',

'maxlag',

'nobs',

'resols',

'usedlag']

-3.183192251191782从漂移项加自回归,或者漂移项+趋势项+自回归都可以看出,模型是平稳的

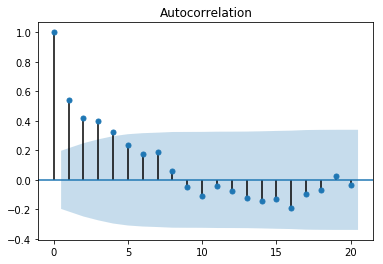

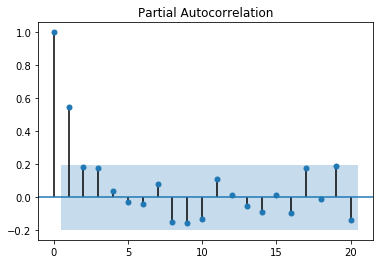

11.2.2.2 序列的纯随机性检验结果

纯随机性检验也就是LB检验,利用Q统计量

因为LB统计量(Q统计量的修正)是利用k阶延迟自相关系数来计算的,所以必须获得前k阶的自相关系数。k一般取6或12

array([ 1. , 0.54173285, 0.41888438, 0.39795532, 0.32404731,

0.23716419, 0.17179424, 0.19022816, 0.06120181, -0.04850548,

-0.10673042, -0.04327143, -0.07230482])array([ 1. , 0.54726074, 0.18276348, 0.17599425, 0.04046234,

-0.02925253, -0.04206131, 0.0784646 , -0.14778847, -0.15651177,

-0.1296911 , 0.113972 , 0.01187113])#计算Q统计量

q_acf=tsa.q_stat(tsa.acf(data.number,nlags=12)[1:],nobs=len(data.number))#用自相关系数计算Q统计量,nobs为总的样本量,而不是自相关的延迟阶数

#q_pacf=tsa.q_stat(tsa.pacf(data.number,nlags=12)[1:],nobs=len(data.number))

q_acf

#q_pacf(array([29.94338136, 48.03065781, 64.52572016, 75.57794735, 81.56105668,

84.73420816, 88.66715745, 89.07872742, 89.34012141, 90.61992405,

90.83267742, 91.43353531]),

array([4.44847764e-08, 3.71770714e-11, 6.33585229e-14, 1.50371504e-15,

3.95511245e-16, 3.74733217e-16, 2.32297279e-16, 7.15231635e-16,

2.20818568e-15, 4.03523693e-15, 1.14482818e-14, 2.60445654e-14]))Help on function q_stat in module statsmodels.tsa.stattools:

q_stat(x, nobs, type='ljungbox')

Return's Ljung-Box Q Statistic

x : array-like

Array of autocorrelation coefficients. Can be obtained from acf.

nobs : int

Number of observations in the entire sample (ie., not just the length

of the autocorrelation function results.

Returns

-------

q-stat : array

Ljung-Box Q-statistic for autocorrelation parameters

p-value : array

P-value of the Q statistic

Notes

-----

Written to be used with acf.#acf,pacf都代表

def suiji(data,nobs,lag=12):

suiji=pd.DataFrame()

suiji['acf']=tsa.acf(data,nlags=lag)[1:]

suiji['pacf']=tsa.pacf(data,nlags=lag)[1:]

suiji['Q']=tsa.q_stat(tsa.acf(data,nlags=lag)[1:],nobs=nobs)[0]

suiji['P']=tsa.q_stat(tsa.acf(data,nlags=lag)[1:],nobs=nobs)[1]

return suiji| acf | pacf | Q | P | |

|---|---|---|---|---|

| 0 | 0.541733 | 0.547261 | 29.943381 | 4.448478e-08 |

| 1 | 0.418884 | 0.182763 | 48.030658 | 3.717707e-11 |

| 2 | 0.397955 | 0.175994 | 64.525720 | 6.335852e-14 |

| 3 | 0.324047 | 0.040462 | 75.577947 | 1.503715e-15 |

| 4 | 0.237164 | -0.029253 | 81.561057 | 3.955112e-16 |

| 5 | 0.171794 | -0.042061 | 84.734208 | 3.747332e-16 |

| 6 | 0.190228 | 0.078465 | 88.667157 | 2.322973e-16 |

| 7 | 0.061202 | -0.147788 | 89.078727 | 7.152316e-16 |

| 8 | -0.048505 | -0.156512 | 89.340121 | 2.208186e-15 |

| 9 | -0.106730 | -0.129691 | 90.619924 | 4.035237e-15 |

| 10 | -0.043271 | 0.113972 | 90.832677 | 1.144828e-14 |

| 11 | -0.072305 | 0.011871 | 91.433535 | 2.604457e-14 |

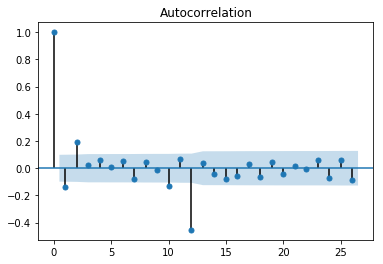

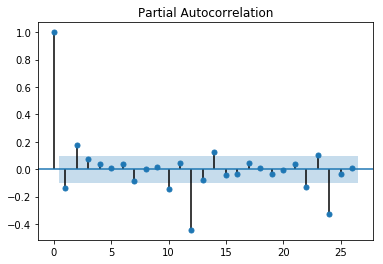

11.2.3 模型构建

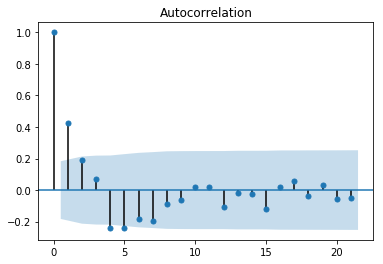

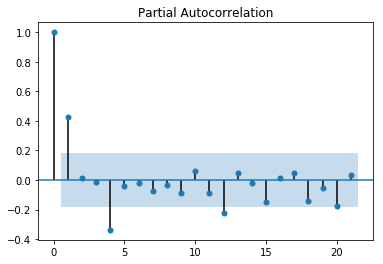

从自相关图可以看出是拖尾的,从偏相关图可以看出是截尾的。阶数为2.所以应该应用AR(2)模型

#导入ar和arma模型的一种方式

from statsmodels.tsa import ar_model

from statsmodels.tsa import arima_model

ar_model.AR

arima_model.ARMAstatsmodels.tsa.ar_model.AR

statsmodels.tsa.arima_model.ARMAstatsmodels.tsa.ar_model.AR

statsmodels.tsa.arima_model.ARMA我们下面只看ARMA的实现,因为AR模型就相当于与ARMA(p,0)

11.2.3.1 模型定阶

#构建arma模型,首先是创建arma模型实例,给与一个时间序列数据

arma_mod20=sm.tsa.ARMA(data,(2,0))#数据是序列或数据框,索引是时间序列数据,并且设置阶数

arma_mod20fit=arma_mod20.fit(disp=-1,trend='c')#这里面可以选择方法和是否添加常数项等。默认有常数项

arma_mod20fit.summary()模型的显著性检验先不看,可以看到参数的检验都是通过的,而通过根的大小(都大于1)我们可以判断出这个AR模型是平稳的。

其实python中还允许利用函数来判断一个arma模型的平稳性和可逆性,from statsmodels.tsa.arima_process import ArmaProcess

但是需要事先构建模型获得系数参数

from statsmodels.tsa.arima_process import ArmaProcess

np.random.seed(1234)

# include zero-th lag

#arma(4,1)

arparams = np.array([1, .75, -.65, -.55, .9])#4阶ar,注意需要包含0阶,这实际上就是自回归系数多项式

maparams = np.array([1, .65])#1阶ma,注意需要包含0阶,这实际上就是系数多项式

arma_t = ArmaProcess(arparams, maparams)#传递ar和ma的系数参数

arma_t.isinvertible#判断可逆性

arma_t.isstationary#判断平稳性True

Falsefig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

ax.plot(arma_t.generate_sample(nsample=50));

另外需要注意的是python中的arma模型不允许构建不平稳的模型,否则会报错。所以我们先在利用bic准则,查看5阶内所有的模型的bic量,对于报错的我们把它的bic定为无穷

p=range(6)

q=range(6)

rank=[]

for i in p:

con=[]

for j in q:

try:

con.append(arima_model.ARMA(data.number,(i,j)).fit(disp=-1).bic)

except:

con.append(np.Inf)

rank.append(con)

rank=pd.DataFrame(rank,index=['AR'+str(i) for i in p],columns=['MA'+str(j) for j in q])

rank| MA0 | MA1 | MA2 | MA3 | MA4 | MA5 | |

|---|---|---|---|---|---|---|

| AR0 | 681.734599 | 662.632218 | 662.113706 | 660.906160 | 662.699747 | 666.007394 |

| AR1 | 651.753037 | 650.836763 | 655.356467 | 658.633388 | 662.940464 | 667.036829 |

| AR2 | 653.114333 | inf | 658.039309 | inf | inf | inf |

| AR3 | 654.472268 | 658.915996 | 663.356277 | 665.307412 | inf | inf |

| AR4 | 658.853051 | 663.431867 | 665.500353 | 670.043316 | inf | inf |

| AR5 | 663.385982 | 665.232821 | 672.597914 | 679.265916 | 671.782722 | inf |

MA0 651.753037

MA1 650.836763

MA2 655.356467

MA3 658.633388

MA4 662.699747

MA5 666.007394

dtype: float64可以看到AR(1,1)模型bic最小,并且模型平稳,我们最终模型定阶为(1,1)

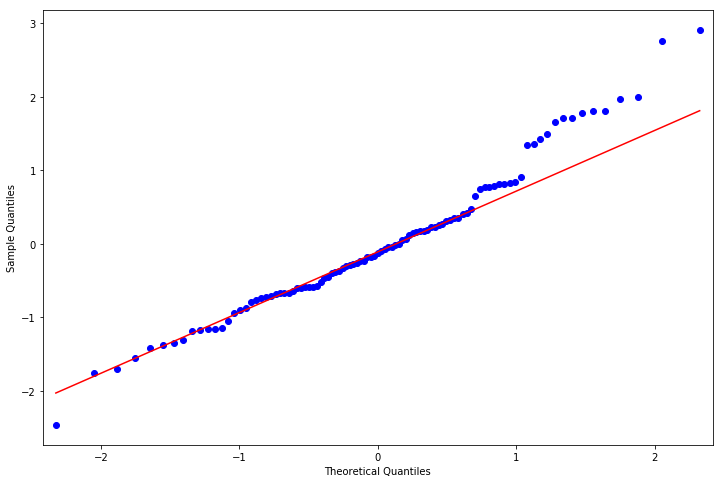

11.2.3.4 正态性检验

from scipy import stats

#正态检验

resid = arma_mod11fit.resid

stats.normaltest(resid)#利用stats包中的正态测试

#利用qq图

from statsmodels.graphics.api import qqplot

fig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

fig = qqplot(resid, line='q', ax=ax, fit=True)NormaltestResult(statistic=5.939742977265384, pvalue=0.051309903814136935)

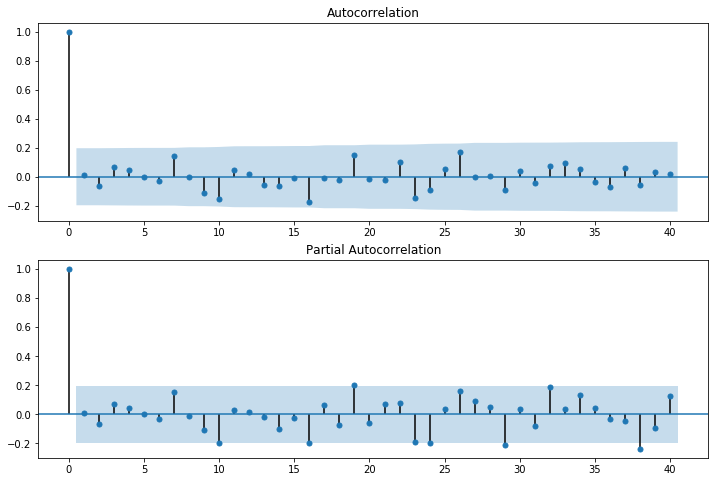

11.2.3.5 随机性检验

即检验模型的显著性

#残差的随机性检验

r,q,p = sm.tsa.acf(resid.values.squeeze(), fft=True, qstat=True)

data1 = np.c_[range(1,41), r[1:], q, p]#默认是40期

table = pd.DataFrame(data1, columns=['lag', "AC", "Q", "Prob(>Q)"])

print(table.set_index('lag'))

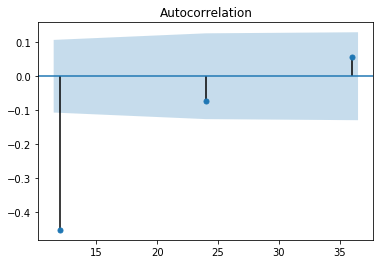

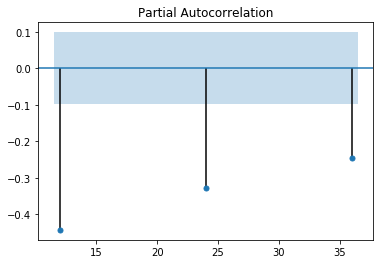

#当残差的随机性检验不通过的时候,可以通过残差的相关图看看还有哪些相关关系未提取干净

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(resid.values.squeeze(), lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(resid, lags=40, ax=ax2) AC Q Prob(>Q)

lag

1.0 0.010300 0.010825 0.917133

2.0 -0.063396 0.425117 0.808513

3.0 0.065777 0.875755 0.831274

4.0 0.047298 1.111215 0.892489

5.0 -0.004223 1.113112 0.952937

6.0 -0.028136 1.198227 0.976972

7.0 0.144325 3.462101 0.839223

8.0 -0.002454 3.462763 0.902060

9.0 -0.113296 4.888849 0.843888

10.0 -0.157036 7.659406 0.662066

11.0 0.045036 7.889868 0.723134

12.0 0.018466 7.929059 0.790649

13.0 -0.056399 8.298885 0.823598

14.0 -0.067152 8.829343 0.841825

15.0 -0.011891 8.846175 0.885422

16.0 -0.171222 12.377992 0.717576

17.0 -0.011226 12.393360 0.775755

18.0 -0.019499 12.440294 0.823693

19.0 0.147969 15.176856 0.711292

20.0 -0.014903 15.204967 0.764562

21.0 -0.023304 15.274586 0.808926

22.0 0.098692 16.539408 0.788244

23.0 -0.148043 19.422915 0.676424

24.0 -0.092072 20.553106 0.664927

25.0 0.050855 20.902567 0.698030

26.0 0.171934 24.951672 0.521712

27.0 -0.003867 24.953749 0.577054

28.0 0.003667 24.955643 0.630249

29.0 -0.088285 26.068993 0.621801

30.0 0.042425 26.329814 0.658196

31.0 -0.039924 26.564193 0.693876

32.0 0.075991 27.425989 0.697433

33.0 0.091602 28.697210 0.681352

34.0 0.053442 29.136551 0.704902

35.0 -0.034872 29.326542 0.738179

36.0 -0.068495 30.071156 0.745837

37.0 0.060894 30.669183 0.759259

38.0 -0.057669 31.214327 0.774112

39.0 0.030721 31.371606 0.802514

40.0 0.020507 31.442874 0.831202

从检验看出残差之间相关性很弱,满足假设

11.2.3.6 预测

利用模型的predict函数和predict_plot函数,可以预测值,以及绘制预测值的图

1980-12-31 17.465377

1981-12-31 18.049009

1982-12-31 16.729012

1983-12-31 14.577349

1984-12-31 15.606044

1985-12-31 13.299255

1986-12-31 15.047666

1987-12-31 12.267820

1988-12-31 13.022072

1989-12-31 12.170360

1990-12-31 11.404516

1991-12-31 13.432397

1992-12-31 13.137112

1993-12-31 18.126782

1994-12-31 17.550478

1995-12-31 16.904956

1996-12-31 20.560380

1997-12-31 20.976142

1998-12-31 20.370293

1999-12-31 18.530631

2000-12-31 18.723334

2001-12-31 18.883399

2002-12-31 19.016353

2003-12-31 19.126788

2004-12-31 19.218519

2005-12-31 19.294713

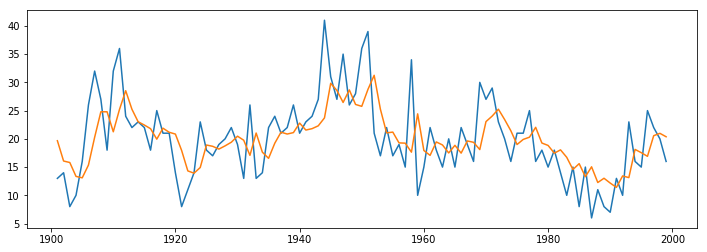

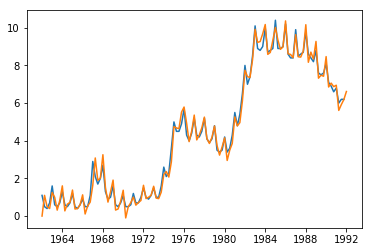

Freq: A-DEC, dtype: float64fig, ax = plt.subplots(figsize=(12, 4))

ax.plot(data)

#arma_mod11fit.plot_predict('2000', '2006',)有问题

ax.plot(arma_mod11fit.predict())[<matplotlib.lines.Line2D at 0x168dd0b0fc8>]

[<matplotlib.lines.Line2D at 0x168dd0b9b88>]

1900-12-31 19.668380

1901-12-31 16.071618

1902-12-31 15.810983

1903-12-31 13.350267

1904-12-31 13.098084

...

1994-12-31 17.550478

1995-12-31 16.904956

1996-12-31 20.560380

1997-12-31 20.976142

1998-12-31 20.370293

Freq: A-DEC, Length: 99, dtype: float64(array([18.5306311 , 18.72333411, 18.8833986 , 19.01635263, 19.12678795]),

array([5.88763837, 6.32759403, 6.61409924, 6.80474257, 6.93322013]),

array([[ 6.99107194, 30.07019026],

[ 6.32147771, 31.12519051],

[ 5.92000229, 31.84679491],

[ 5.67930228, 32.35340298],

[ 5.5379262 , 32.7156497 ]]))1999-12-31 18.530631

2000-12-31 18.723334

2001-12-31 18.883399

2002-12-31 19.016353

2003-12-31 19.126788

2004-12-31 19.218519

2005-12-31 19.294713

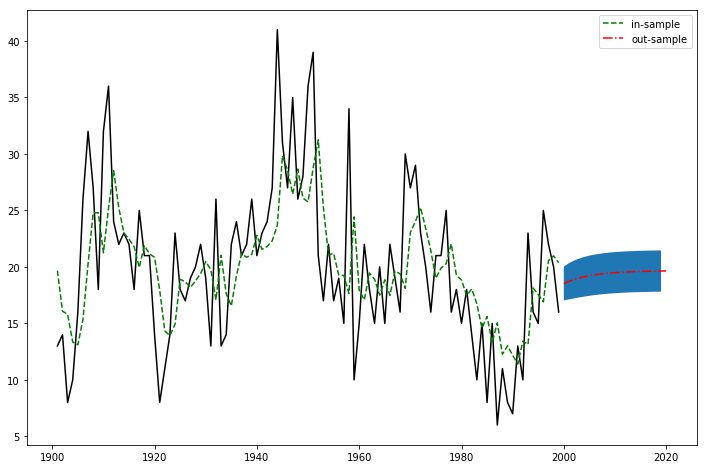

Freq: A-DEC, dtype: float64fig,ax=plt.subplots(figsize=(12,8))

ax.plot(data,color='black')

ax.plot(arma_mod11fit.predict(),ls='--',color='green',label='in-sample')

ax.plot(arma_mod11fit.predict('1999','2019'),ls='-.',color='red',label='out-sample')

l,r=arma_mod11fit.forecast(20,alpha=0.8)[2][:,0],arma_mod11fit.forecast(20,alpha=0.8)[2][:,1]

ax.fill_between(pd.date_range('1999','2019',freq='a'),l,r)

ax.legend()[<matplotlib.lines.Line2D at 0x168dcd2dac8>]

[<matplotlib.lines.Line2D at 0x168dcd4c1c8>]

[<matplotlib.lines.Line2D at 0x168dcd4cb48>]

<matplotlib.collections.PolyCollection at 0x168dcd51ec8>

<matplotlib.legend.Legend at 0x168dcd51f88>

Help on method forecast in module statsmodels.tsa.arima_model:

forecast(steps=1, exog=None, alpha=0.05) method of statsmodels.tsa.arima_model.ARMAResults instance

Out-of-sample forecasts

Parameters

----------

steps : int

The number of out of sample forecasts from the end of the

sample.

exog : array

If the model is an ARMAX, you must provide out of sample

values for the exogenous variables. This should not include

the constant.

alpha : float

The confidence intervals for the forecasts are (1 - alpha) %

Returns

-------

forecast : array

Array of out of sample forecasts

stderr : array

Array of the standard error of the forecasts.

conf_int : array

2d array of the confidence interval for the forecastHelp on method predict in module statsmodels.tsa.arima_model:

predict(start=None, end=None, exog=None, dynamic=False) method of statsmodels.tsa.arima_model.ARMAResultsWrapper instance

predict(self, start=None, end=None, exog=None, dynamic=False)

ARMA model in-sample and out-of-sample prediction

Parameters

----------

start : int, str, or datetime

Zero-indexed observation number at which to start forecasting, ie.,

the first forecast is start. Can also be a date string to

parse or a datetime type.

end : int, str, or datetime

Zero-indexed observation number at which to end forecasting, ie.,

the first forecast is start. Can also be a date string to

parse or a datetime type. However, if the dates index does not

have a fixed frequency, end must be an integer index if you

want out of sample prediction.

exog : array-like, optional

If the model is an ARMAX and out-of-sample forecasting is

requested, exog must be given. Note that you'll need to pass

`k_ar` additional lags for any exogenous variables. E.g., if you

fit an ARMAX(2, q) model and want to predict 5 steps, you need 7

observations to do this.

dynamic : bool, optional

The `dynamic` keyword affects in-sample prediction. If dynamic

is False, then the in-sample lagged values are used for

prediction. If `dynamic` is True, then in-sample forecasts are

used in place of lagged dependent variables. The first forecasted

value is `start`.

Returns

-------

predict : array

The predicted values.

Notes

-----

It is recommended to use dates with the time-series models, as the

below will probably make clear. However, if ARIMA is used without

dates and/or `start` and `end` are given as indices, then these

indices are in terms of the *original*, undifferenced series. Ie.,

given some undifferenced observations::

1970Q1, 1

1970Q2, 1.5

1970Q3, 1.25

1970Q4, 2.25

1971Q1, 1.2

1971Q2, 4.1

1970Q1 is observation 0 in the original series. However, if we fit an

ARIMA(p,1,q) model then we lose this first observation through

differencing. Therefore, the first observation we can forecast (if

using exact MLE) is index 1. In the differenced series this is index

0, but we refer to it as 1 from the original series.11.2.3.7 生成相应系数的arma模型以及样本

## 利用from statsmodels.tsa.arima_process import ArmaProcess

arpar=np.r_[1,-arma_mod11fit.arparams]#注意负号

maapr=np.r_[1,arma_mod11fit.maparams]

arma_t=ArmaProcess(arpar,maapr)

arma_t.generate_sample(50)#生成样本数array([ 0.84100879, -1.11466772, -1.69619658, -0.89732715, -1.24949787,

-0.9429691 , -0.36605419, -0.49423353, 0.17072922, 1.44030944,

-0.45314823, -0.0211145 , 0.32116309, -0.07627831, 1.06153154,

-1.97036659, 1.44268116, -0.83143763, 0.02046505, 0.62915108,

-0.57072571, 0.33114286, 0.77741837, 0.86158753, -0.43930777,

2.04760704, 1.05056826, -0.37918406, 0.82059652, 0.44502154,

0.81677717, -3.08796419, 0.31299866, -0.16455348, -0.03883496,

-0.53423336, 0.5115214 , 1.07455292, 0.73309407, 1.88259081,

1.0354387 , 0.42521786, -0.49991477, -0.55091025, 0.61444634,

0.07167267, -0.24943137, 0.47172613, -0.90796036, -0.79903477])['__class__',

'__delattr__',

'__dict__',

'__dir__',

'__doc__',

'__eq__',

'__format__',

'__ge__',

'__getattribute__',

'__gt__',

'__hash__',

'__init__',

'__init_subclass__',

'__le__',

'__lt__',

'__module__',

'__mul__',

'__ne__',

'__new__',

'__reduce__',

'__reduce_ex__',

'__repr__',

'__setattr__',

'__sizeof__',

'__str__',

'__subclasshook__',

'__weakref__',

'acf',

'acovf',

'ar',

'arcoefs',

'arma2ar',

'arma2ma',

'arpoly',

'arroots',

'from_coeffs',

'from_estimation',

'generate_sample',

'impulse_response',

'invertroots',

'isinvertible',

'isstationary',

'ma',

'macoefs',

'mapoly',

'maroots',

'nobs',

'pacf',

'periodogram']生成相应模型后,可以计算模型的自相关,偏自相关,自协方差函数等

array([1. , 0.53937576, 0.44802054, 0.37213835, 0.30910848,

0.25675412, 0.21326713, 0.17714562, 0.14714209, 0.12222032,

0.1015196 , 0.08432501])

array([1.00000000e+00, 5.39375760e-01, 2.21548631e-01, 9.56983544e-02,

4.17191583e-02, 1.82189418e-02, 7.95893463e-03, 3.47707644e-03,

1.51907351e-03, 6.63658016e-04, 2.89941305e-04, 1.26670613e-04])

array([1.50001883, 0.8090738 , 0.67203925, 0.55821453, 0.46366854,

0.38513601, 0.31990471, 0.26572176, 0.2207159 , 0.18333278,

0.15228132, 0.12648911])array([ 0.29120536, 0.68119412, 0.82190127, 0.74797878, 0.98093912,

1.96669932, 0.25680721, 0.08654568, 1.50093088, -0.56938977,

0.96221975, -1.29394972, -0.77817225, 0.29972415, -0.28227105,

-0.32754268, 0.48817939, -1.71037106, -0.57913776, -0.10676858,

-0.509618 , -0.93247366, -1.18755667, -0.25181921, -2.10277464,

-0.60889419, -1.15709421, -1.05072217, -0.0480205 , 0.33550013,

0.22174955, 0.23075989, 0.94173438, 2.31921265, 1.73878118,

0.20280618, -1.49651451, 1.59821857, -1.25111724, 0.9293164 ,

1.04055467, 0.13611643, 0.98155745, -0.34197525, 1.26426066,

0.01166392, 0.93966998, 1.45848901, 0.65975754, 2.96696278])#验证一下确实是模型的自相关,偏自相关

# 生成一个平稳arma(1,0)模型

ar1=np.array([1,0.8])

ma1=np.array([1])

arma20=ArmaProcess(ar1,ma1)

arma20.acf(12)#ar(1)模型的k阶自相关应该是系数的k次方

arma20.pacf(12)#除了1阶为系数,其他皆为0

np.array([0.8**i for i in range(12)])

#验证是通过的array([ 1. , -0.8 , 0.64 , -0.512 , 0.4096 ,

-0.32768 , 0.262144 , -0.2097152 , 0.16777216, -0.13421773,

0.10737418, -0.08589935])

array([ 1.00000000e+00, -8.00000000e-01, -3.45402719e-16, -6.16790569e-17,

4.31753398e-17, -3.25171988e-17, -1.04854397e-16, 7.70988212e-17,

1.23358114e-17, -4.62592927e-17, -1.38777878e-17, 1.07938350e-17])

array([1. , 0.8 , 0.64 , 0.512 , 0.4096 ,

0.32768 , 0.262144 , 0.2097152 , 0.16777216, 0.13421773,

0.10737418, 0.08589935])11.2.3.8 模型定阶的简便方法

设置最大和最小AR、MA阶数,给与data和信息准则,信息准则可以是一个字符串或一个列表,同时可以选择是否中心化。检测后,可以利用.aic_min_order或.bic_min_order等你选择的最小准则选择最佳的模型,并且模型一定是平稳和可逆的。不满足的无值

Help on function arma_order_select_ic in module statsmodels.tsa.stattools:

arma_order_select_ic(y, max_ar=4, max_ma=2, ic='bic', trend='c', model_kw=None, fit_kw=None)

Returns information criteria for many ARMA models

Parameters

----------

y : array-like

Time-series data

max_ar : int

Maximum number of AR lags to use. Default 4.

max_ma : int

Maximum number of MA lags to use. Default 2.

ic : str, list

Information criteria to report. Either a single string or a list

of different criteria is possible.

trend : str

The trend to use when fitting the ARMA models.

model_kw : dict

Keyword arguments to be passed to the ``ARMA`` model

fit_kw : dict

Keyword arguments to be passed to ``ARMA.fit``.

Returns

-------

obj : Results object

Each ic is an attribute with a DataFrame for the results. The AR order

used is the row index. The ma order used is the column index. The

minimum orders are available as ``ic_min_order``.

Examples

--------

>>> from statsmodels.tsa.arima_process import arma_generate_sample

>>> import statsmodels.api as sm

>>> import numpy as np

>>> arparams = np.array([.75, -.25])

>>> maparams = np.array([.65, .35])

>>> arparams = np.r_[1, -arparams]

>>> maparam = np.r_[1, maparams]

>>> nobs = 250

>>> np.random.seed(2014)

>>> y = arma_generate_sample(arparams, maparams, nobs)

>>> res = sm.tsa.arma_order_select_ic(y, ic=['aic', 'bic'], trend='nc')

>>> res.aic_min_order

>>> res.bic_min_order

Notes

-----

This method can be used to tentatively identify the order of an ARMA

process, provided that the time series is stationary and invertible. This

function computes the full exact MLE estimate of each model and can be,

therefore a little slow. An implementation using approximate estimates

will be provided in the future. In the meantime, consider passing

{method : 'css'} to fit_kw.{'aic': 0 1 2 3 4

0 NaN 799.674173 761.067479 738.361676 715.759799

1 666.645525 647.132300 648.738566 649.986452 651.941850

2 656.028374 648.842840 648.850644 650.846599 652.699837

3 649.748166 650.009945 652.004944 NaN 654.552222

4 650.228277 652.004611 NaN 651.799867 654.256041,

'bic': 0 1 2 3 4

0 NaN 804.864412 768.852838 748.742155 728.735398

1 671.835765 654.917660 659.119046 662.962051 667.512569

2 663.813734 659.223319 661.826244 666.417318 670.865676

3 660.128646 662.985544 667.575663 NaN 675.313181

4 663.203877 667.575330 NaN 672.560826 677.612119,

'aic_min_order': (1, 1),

'bic_min_order': (1, 1)}['__class__',

'__contains__',

'__delattr__',

'__delitem__',

'__dict__',

'__dir__',

'__doc__',

'__eq__',

'__format__',

'__ge__',

'__getattribute__',

'__getitem__',

'__gt__',

'__hash__',

'__init__',

'__init_subclass__',

'__iter__',

'__le__',

'__len__',

'__lt__',

'__module__',

'__ne__',

'__new__',

'__reduce__',

'__reduce_ex__',

'__repr__',

'__setattr__',

'__setitem__',

'__sizeof__',

'__str__',

'__subclasshook__',

'__weakref__',

'aic',

'aic_min_order',

'bic',

'bic_min_order',

'clear',

'copy',

'fromkeys',

'get',

'items',

'keys',

'pop',

'popitem',

'setdefault',

'update',

'values']dict_keys(['aic', 'bic', 'aic_min_order', 'bic_min_order'])11.2.4 模型总结

sm.tsa=tsa

| 步骤 | 方法 | 解释 |

|---|---|---|

| 模型定阶 | sm.tsa.arma_order_select_ic(data,max_ar,max_ma,ic,trend,model_kw,fit_kw) |

data:数据 max_ar,max_ma:最大的阶数 ic:字符串或者列表,指定信息准则 trend:‘c’or‘nc’,是否中心化 model_kw,fit_kw:arma以及arma.fit的参数 |

| 模型构建 | 按照数据和阶数构建:arma_mod=sm.tsa.ARMA(data)arma_modfit=arma_mod.fit(disp=-1,trend='c')

|

arma_mod的参数一般只需要输入data,序列或数据框,索引为时间类型。 fit的时候可以选择计算方法,是否包含常数项等. 通过summary方法可以看到模型的信息量,参数的检验结果,系数,系数多项式的根。 还有其他属性可以获得参数值,ar或ma参数,ar或ma的根,信息量,残差等。 但是无法计算模型的协方差等信息 |

| - | 按照ar和ma的系数构建,注意即延迟算子形式的系数from sm.tsa.arima_process import ArmaProcessArmaProcess(ar,ma)

|

ar:ar的所有系数 ma:ma的所有系数 此模型也可以获得ar,ma等系数,根 同时还可以获取模型的自协方差,自相关系数等 同时还可以检验模型的可逆性和稳定性 同时还可以获得模型的逆转形式的系数多项式的根 |

| 生成相应模型样本(非必要步骤) |

sm.tsa.arma.generate_sample(ar,ma,nobs)或AramaProcess(ar,ma).generate_sample(nsample)

|

可以直接调用函数,也可以通过先生成模型再进行生成样本 |

| 检验模型 | 模型的显著性检验:r,q,p = sm.tsa.acf(resid, fft=True, qstat=True)默认nlags40残差的相关性检验: sm.stats.durbin_watson(arma_mod11fit.resid.values)残差的正态性检验: scipy.stats.normaltest(resid)模型的参数检验:在生成模型的时候就已经可以判断,如果有参数被舍弃,则应重新建模 |

r,q,p代表自相关值,q统计量值,p值,判断残差随机性 dw检验也检验残差的相关性 正态检验还可以通过 statsmodels.graphics.api.qqplot(resid, line='q', ax=ax, fit=True)判断拟合效果 |

| 模型预测 | .predict(开始时间,结束时间) |

注意不要设置dynamic=True,否则预测值会近似一条直线 可以将预测值和样本值放在一起比较结果 |

11.2.6 ARIMA 非平稳无季节效应时间序列

当时间序列非平稳但是不存在其他诸如季节效应的随机影响时,一般只需要做差分就可以获得平稳序列。可能是一阶,二阶,并且可以证明d阶差分后一定是平稳的,但是差分阶数越高,方差越大,所以我们要选择合适的差分阶数。避免出现过差分现象

其实差分就是自回归,一个差分可以写成自回归的形式,就是用自回归来提取序列中蕴含的确定性信息

对蕴含固定周期的序列进行步长为周期长度的差分运算,(k步差分)通常可以可以很好的提取周期信息,这和有季节因素的非平稳序列比较有关系

ARIMA(p,d,q)p,q和ARMA模型一致,d代表做几阶差分。当p=q=0,d=0时,\(x_t=x_{t-1}+\epsilon\),称为随机游走模型或醉汉模型

arima_mod=tsa.SARIMAX(data,order=(p,d,q))

arima_modpdq=arima_modpdq.fit(disp=-1)11.2.6.1 数据是否平稳

import requests

from io import BytesIO

wpi1 = requests.get('https://www.stata-press.com/data/r12/wpi1.dta').content

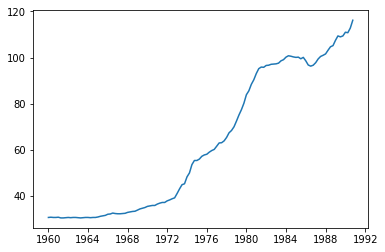

data = pd.read_stata(BytesIO(wpi1))

data.index = data.t| wpi | t | ln_wpi | |

|---|---|---|---|

| t | |||

| 1960-01-01 | 30.700001 | 1960-01-01 | 3.424263 |

| 1960-04-01 | 30.799999 | 1960-04-01 | 3.427515 |

| 1960-07-01 | 30.700001 | 1960-07-01 | 3.424263 |

| 1960-10-01 | 30.700001 | 1960-10-01 | 3.424263 |

| 1961-01-01 | 30.799999 | 1961-01-01 | 3.427515 |

| … | … | … | … |

| 1989-10-01 | 109.400002 | 1989-10-01 | 4.695011 |

| 1990-01-01 | 111.000000 | 1990-01-01 | 4.709530 |

| 1990-04-01 | 110.800003 | 1990-04-01 | 4.707727 |

| 1990-07-01 | 112.800003 | 1990-07-01 | 4.725616 |

| 1990-10-01 | 116.199997 | 1990-10-01 | 4.755313 |

124 rows × 3 columns

[<matplotlib.lines.Line2D at 0x168dd8d7848>]

可以判断大致应该是做一阶差分

11.2.6.2 差分并做单位根检验

def select_arima_orderd_adf(data,maxlag):

results=[tsa.adfuller(data.diff(i).dropna())[1] for i in range(1,maxlag+1)]

results=pd.DataFrame(results,index=range(1,maxlag+1),columns=['p值'])

results._set_axis_name('差分阶数',inplace=True)

return results| p值 | |

|---|---|

| 差分阶数 | |

| 1 | 0.098945 |

| 2 | 0.121322 |

| 3 | 0.069117 |

| 4 | 0.359309 |

| 5 | 0.122730 |

这里其实全部都没有通过0.05的检验,那我们就取0.1为标准,所以一阶差分就可

11.2.6.3 构建ARIMA模型

#首先获取差分数据

data['d1wpi']=data['wpi'].diff()

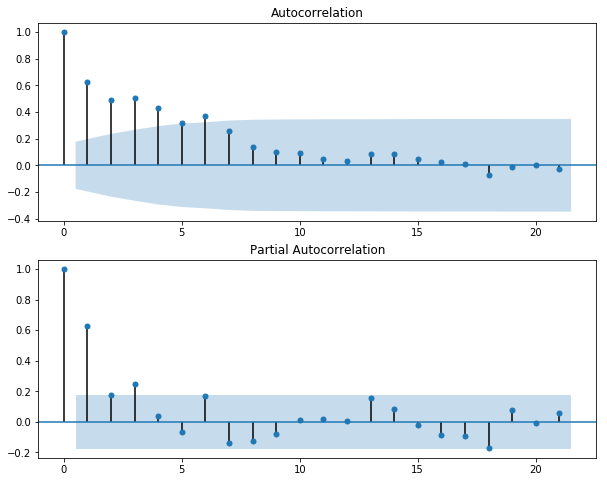

#绘制相关图。判断p,q

fig=plt.figure(figsize=(10,8))

ax1=plt.subplot(211);plot_acf(data.d1wpi.dropna(),ax=ax1).show()

ax2=plt.subplot(212);plot_pacf(data.d1wpi.dropna(),ax=ax2).show()

根据自相关图和偏相关图,我们也可以判断是否适合用疏系数模型

{'aic': 0 1 2 3 4

0 347.072562 307.552197 299.357225 293.948300 285.064261

1 283.806987 278.702628 280.105905 280.726991 281.041604

2 281.855956 280.368858 281.696667 279.304674 280.894012

3 278.371786 280.281285 NaN 304.722568 279.878126

4 280.205568 279.706951 279.272632 280.581639 281.139270,

'bic': 0 1 2 3 4

0 352.696930 315.988750 310.605962 308.009222 301.937367

1 292.243540 289.951365 294.166827 297.600097 300.726894

2 293.104694 294.429780 298.569774 298.989965 303.391487

3 292.432708 297.154391 NaN 327.220043 305.187785

4 297.078674 299.392241 301.770106 305.891298 309.261113,

'aic_min_order': (3, 0),

'bic_min_order': (1, 1)}使用bic准则我们p=1,q=1

11.2.6.5 预测

1960-01-01 0.749786

1960-04-01 31.449807

1960-07-01 31.122188

1960-10-01 30.867851

1961-01-01 30.862600

...

1990-01-01 109.912121

1990-04-01 112.044809

1990-07-01 111.232380

1990-10-01 113.996828

1991-01-01 118.358861

Freq: QS-OCT, Length: 125, dtype: float64<statsmodels.tsa.statespace.mlemodel.PredictionResultsWrapper at 0x168debe0c48>| lower wpi | upper wpi | |

|---|---|---|

| 1960-01-01 | -1959.215181 | 1960.714753 |

| 1960-04-01 | 29.487836 | 33.411777 |

| 1960-07-01 | 29.644898 | 32.599478 |

| 1960-10-01 | 29.437815 | 32.297886 |

| 1961-01-01 | 29.440036 | 32.285163 |

| … | … | … |

| 1989-10-01 | 108.144279 | 110.986387 |

| 1990-01-01 | 108.491066 | 111.333175 |

| 1990-04-01 | 110.623755 | 113.465863 |

| 1990-07-01 | 109.811325 | 112.653434 |

| 1990-10-01 | 112.575774 | 115.417882 |

124 rows × 2 columns

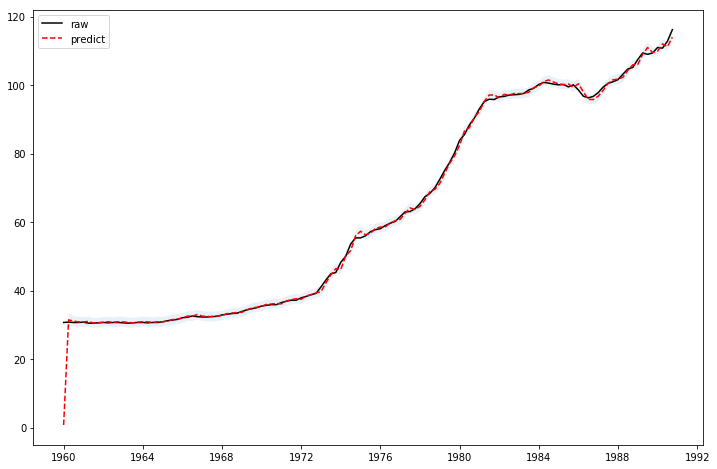

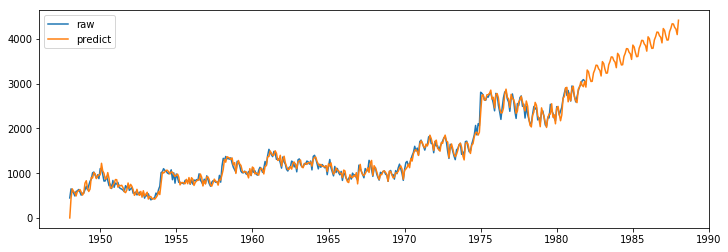

fig,ax=plt.subplots(figsize=(12,8))

ax.plot(data.wpi,'k',label='raw')

ax.plot(arima_mod111fit.predict(),'r--',label='predict')

ci=arima_mod111fit.get_prediction().conf_int().iloc[1:,]

l,r=ci.iloc[:,0],ci.iloc[:,1]

ax.fill_between(ci.index,l,r,alpha=0.1)

ax.legend()

plt.show()[<matplotlib.lines.Line2D at 0x168de9d5c88>]

[<matplotlib.lines.Line2D at 0x168de9f0508>]

<matplotlib.collections.PolyCollection at 0x168debee508>

<matplotlib.legend.Legend at 0x168de9f59c8>

11.2.7 有季节效应的非平稳模型

- 直接差分,先消掉趋势。再按照周期来构建疏系数模型,季度数据,月度数据周期是一年

- arima加法和乘法模型

- x11季节调节模型

- 指数平滑模型

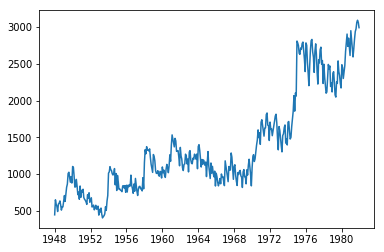

# Dataset

data = pd.read_stata(BytesIO(wpi1))

data.index = data.t

data['ln_wpi'] = np.log(data['wpi'])

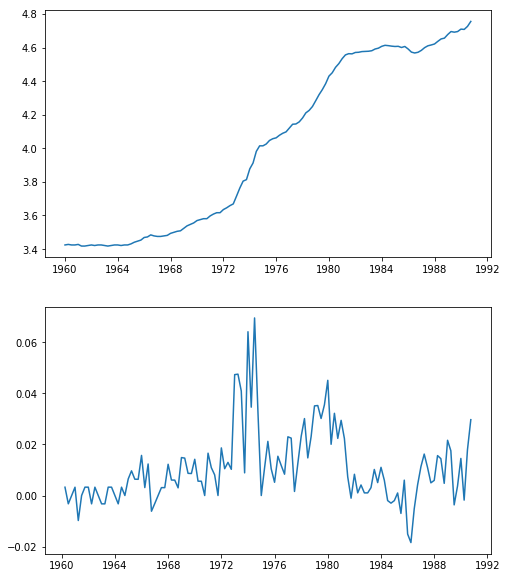

data['D.ln_wpi'] = data['ln_wpi'].diff()#注意这里的时间之间差值是三个月,也就是季度数据,那我们在构建时只需构建滞后四期fig=plt.figure(figsize=(8,10))

ax1=plt.subplot(211);ax1.plot(data.ln_wpi)

ax2=plt.subplot(212);ax2.plot(data['D.ln_wpi'])[<matplotlib.lines.Line2D at 0x168dee1dc88>]

[<matplotlib.lines.Line2D at 0x168dee32c88>]

11.2.7.1 第一种模型构建

ar = 1 # this is the maximum degree specification

ma = (1,0,0,1) # this is the lag polynomial specification

mod = tsa.SARIMAX(data['wpi'], trend='c', order=(ar,1,ma))#这里把关于时间t的函数就设置为常数c

modfit=mod.fit(disp=-1)

modfit.summary()#应为该序列并没有季节效应,四阶滞后参数检验不通过| x | |

|---|---|

| time | |

| 1948-01-01 | 446 |

| 1948-02-01 | 650 |

| 1948-03-01 | 592 |

| 1948-04-01 | 561 |

| 1948-05-01 | 491 |

| … | … |

| 1981-08-01 | 2975 |

| 1981-09-01 | 3064 |

| 1981-10-01 | 3092 |

| 1981-11-01 | 3063 |

| 1981-12-01 | 2991 |

408 rows × 1 columns

[<matplotlib.lines.Line2D at 0x168deaa9448>]

| p值 | |

|---|---|

| 差分阶数 | |

| 1 | 5.224534e-06 |

| 2 | 1.957925e-07 |

| 3 | 5.315701e-07 |

11.2.7.2 ARIMA加法模型

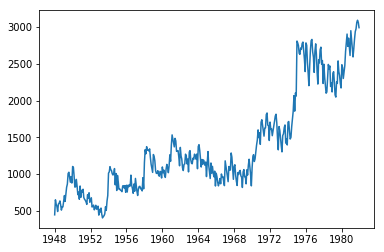

加法模型其实就是先获得平稳的模型,将不稳定因素减去,对剩下的因素构建适当的ARMA模型

| x | |

|---|---|

| time | |

| 1962-01-01 | 1.1 |

| 1962-04-01 | 0.5 |

| 1962-07-01 | 0.4 |

| 1962-10-01 | 0.7 |

| 1963-01-01 | 1.6 |

| … | … |

| 1990-10-01 | 6.6 |

| 1991-01-01 | 6.8 |

| 1991-04-01 | 6.0 |

| 1991-07-01 | 6.2 |

| 1991-10-01 | 6.2 |

120 rows × 1 columns

[<matplotlib.lines.Line2D at 0x168de935808>]

#做一阶差分和4步差分,得到数据,因为这是季度数据

dx=data['x'].diff().dropna()

dx12=pd.Series([n-dx[::-1][i+4] for i,n in enumerate(dx[::-1]) if i+4<len(dx)])(-6.15621309726213,

7.357953744299023e-08,

3,

111,

{'1%': -3.490683082754047,

'5%': -2.8879516565798817,

'10%': -2.5808574442009578},

57.66176611874175)

array([[ 4.22066251e-01, 2.10251984e+01, 4.53282432e-06],

[ 1.88976812e-01, 2.52774828e+01, 3.24387684e-06],

[ 7.24845218e-02, 2.59086671e+01, 9.96671089e-06],

[-2.38843592e-01, 3.28235991e+01, 1.29804479e-06],

[-2.38793298e-01, 3.97984557e+01, 1.63984012e-07],

[-1.80874879e-01, 4.38368964e+01, 7.96352503e-08],

[-1.94932404e-01, 4.85708939e+01, 2.75329616e-08],

[-8.88521849e-02, 4.95636354e+01, 4.95665651e-08],

[-5.97374814e-02, 5.00166077e+01, 1.06952006e-07],

[ 2.17768244e-02, 5.00773769e+01, 2.58303768e-07],

[ 2.17725542e-02, 5.01387063e+01, 5.91003399e-07],

[-1.09621764e-01, 5.17084909e+01, 6.98214396e-07],

[-2.03836243e-02, 5.17632992e+01, 1.48118422e-06],

[-2.72508298e-02, 5.18622277e+01, 2.96709626e-06],

[-1.20310925e-01, 5.38098011e+01, 2.82621187e-06],

[ 1.71314533e-02, 5.38496887e+01, 5.48699630e-06],

[ 5.63344292e-02, 5.42854066e+01, 8.91900867e-06],

[-3.70409246e-02, 5.44757227e+01, 1.54678157e-05],

[ 3.34272080e-02, 5.46323302e+01, 2.64565501e-05],

[-5.67773727e-02, 5.50889037e+01, 3.98239366e-05],

[-4.87304255e-02, 5.54288077e+01, 6.12018160e-05],

[-7.49039463e-03, 5.54369250e+01, 1.02921942e-04],

[-1.15397953e-01, 5.73844905e+01, 9.04122266e-05],

[-1.17972793e-01, 5.94423041e+01, 7.65404775e-05],

[-4.28970359e-02, 5.97174074e+01, 1.14349898e-04],

[-6.39266238e-02, 6.03352207e+01, 1.51143632e-04],

[ 5.67403641e-02, 6.08274702e+01, 2.05279762e-04],

[ 1.22109796e-01, 6.31335029e+01, 1.59611818e-04],

[ 8.42926928e-02, 6.42451453e+01, 1.77948161e-04],

[ 1.39901237e-01, 6.73433341e+01, 1.09119067e-04],

[ 2.38312186e-01, 7.64403073e+01, 1.03975215e-05],

[ 2.14123950e-01, 8.38728276e+01, 1.56253569e-06],

[ 1.36469084e-01, 8.69287224e+01, 9.62407575e-07],

[ 7.75446317e-03, 8.69387110e+01, 1.59550939e-06],

[-1.75615070e-01, 9.21257233e+01, 4.93164324e-07],

[-1.93746705e-01, 9.85190259e+01, 1.01272609e-07],

[-2.27914085e-01, 1.07479509e+02, 8.53842148e-09],

[-9.94686998e-02, 1.09208393e+02, 8.27441070e-09],

[ 1.02066788e-02, 1.09226836e+02, 1.42176837e-08],

[-1.57033533e-02, 1.09271076e+02, 2.39135167e-08]])#检验通过,在绘制自相关图加上order选择,判断最终定阶

plot_acf(dx12).show()

plot_pacf(dx12).show()

tsa.arma_order_select_ic(dx12,3,3,ic='bic'){'bic': 0 1 2 3

0 96.453316 80.919882 84.974043 80.342909

1 78.398369 83.123195 87.789872 84.874616

2 83.121046 87.865584 80.724535 83.286027

3 87.847277 81.027281 85.840942 92.948794, 'bic_min_order': (1, 0)}

结合自相关图和偏自相关图,可以看到除了一阶和四阶,其他的都在两倍标准差内。所以可以尝试拟合疏系数模型,并且根据拖尾和截尾性质,使用ar模型.加法模型

\(ARIMA((1,4),(1,4),0)\)=\(ARIMA(1,1,0)\times(0,1,0)_4\)

ar=[1,0,0,1]

mod=tsa.SARIMAX(data,order=(ar,1,0),seasonal_order=(0,1,0,4))

modfit=mod.fit(disp=-1)

modfit.summary()1962-01-01 0.000000

1962-04-01 1.100000

1962-07-01 0.500000

1962-10-01 0.400000

1963-01-01 1.250000

...

1991-01-01 6.949265

1991-04-01 5.612139

1991-07-01 5.916173

1991-10-01 6.186753

1992-01-01 6.615064

Freq: QS-OCT, Length: 121, dtype: float64[<matplotlib.lines.Line2D at 0x168dc191608>]

[<matplotlib.lines.Line2D at 0x168de924208>]

季节的加法模型和上面一个模型相比就是多了一个季节参数,也就是一个季节的k步差分

模型检验

都是通过的

略

11.2.7.3 ARIMA乘法模型

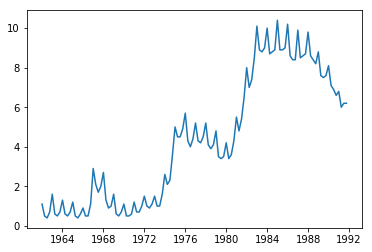

[<matplotlib.lines.Line2D at 0x168dba2ca88>]| x | |

|---|---|

| time | |

| 1948-01-01 | 446 |

| 1948-02-01 | 650 |

| 1948-03-01 | 592 |

| 1948-04-01 | 561 |

| 1948-05-01 | 491 |

| … | … |

| 1981-08-01 | 2975 |

| 1981-09-01 | 3064 |

| 1981-10-01 | 3092 |

| 1981-11-01 | 3063 |

| 1981-12-01 | 2991 |

408 rows × 1 columns

#先将趋势项和季节效应提取,检验序列是否是平稳非白噪声序列

#刚刚做一阶差分后已经提取了趋势效应

#再做12步差分,提取季节效应

dx=data['x'].diff().dropna()

dx12=pd.Series([n-dx[::-1][i+12] for i,n in enumerate(dx[::-1]) if i+12<len(dx)])#然后再确定是否是白噪声序列

r,q,p=tsa.acf(data['x'].diff().dropna(),fft=True,qstat=True,nlags=12)

np.c_[r[1:],q,p]array([[-1.85749784e-01, 1.41464777e+01, 1.69113428e-04],

[ 2.98935223e-03, 1.41501507e+01, 8.45928814e-04],

[-2.60302718e-01, 4.20687586e+01, 3.87956739e-09],

[-7.06041807e-02, 4.41278399e+01, 6.03523844e-09],

[ 2.35100467e-01, 6.70153553e+01, 4.27733608e-13],

[-1.54958260e-02, 6.71150341e+01, 1.59431485e-12],

[ 2.03394043e-01, 8.43311106e+01, 1.79654981e-15],

[-8.43815734e-02, 8.73016825e+01, 1.63938501e-15],

[-2.42222914e-01, 1.11841148e+02, 6.20008961e-20],

[-7.56589124e-02, 1.14241348e+02, 7.42517345e-20],

[-1.13345720e-01, 1.19641833e+02, 2.14011551e-20],

[ 6.13800469e-01, 2.78414249e+02, 1.57763769e-52]])#可以判断不是白噪声,为模型定阶

tsa.arma_order_select_ic(dx12,3,3,'bic')

plot_acf(dx12).show()

plot_pacf(dx12).show(){'bic': 0 1 2 3

0 4860.959171 4861.392903 4852.740094 4858.431293

1 4859.319573 4859.251978 4857.639464 4863.045988

2 4853.259759 4856.594373 4862.554521 4868.222488

3 4857.194729 4862.560040 4856.715196 4860.269284,

'bic_min_order': (0, 2)}

# 模型尝试

ar=[0]*12

ar[0]=1

ar[-1]=1

ma=[0]*12

ma[0]=1

ma[1]=1

ma[-1]=1

## AR(1,12)

r,q,p=tsa.acf(tsa.SARIMAX(data,order=(ar,1,0),seasonal_order=(0,1,0,12)).fit(disp=-1).resid,fft=True,qstat=True,nlags=12)

np.c_[r[1:],q,p]

##MA(1,2,12)

r,q,p=tsa.acf(tsa.SARIMAX(data,order=(0,1,ma),seasonal_order=(0,1,0,12)).fit(disp=-1).resid,fft=True,qstat=True,nlags=12)

np.c_[r[1:],q,p]

##ARMA((1,12),(1,12))

r,q,p=tsa.acf(tsa.SARIMAX(data,order=(ar,1,ar),seasonal_order=(0,1,0,12)).fit(disp=-1).resid,fft=True,qstat=True,nlags=12)

np.c_[r[1:],q,p]array([[ 2.62090931e-04, 2.82327771e-05, 9.95760498e-01],

[ 1.59764475e-01, 1.05167024e+01, 5.20387781e-03],

[ 6.39902758e-04, 1.05168715e+01, 1.46468835e-02],

[ 6.61403669e-02, 1.23281943e+01, 1.50705147e-02],

[ 2.91205772e-02, 1.26801913e+01, 2.65673310e-02],

[ 5.60074868e-02, 1.39854907e+01, 2.97986615e-02],

[-7.44858289e-02, 1.62999362e+01, 2.25130010e-02],

[ 4.75763942e-02, 1.72465374e+01, 2.76418710e-02],

[ 1.67598772e-03, 1.72477151e+01, 4.49751787e-02],

[-8.53212637e-02, 2.03073916e+01, 2.64757342e-02],

[ 4.68050874e-02, 2.12304722e+01, 3.10604125e-02],

[-1.90425816e-01, 3.65484165e+01, 2.64346585e-04]])

array([[-4.38793784e-03, 7.91353530e-03, 9.29115246e-01],

[ 1.08908145e-01, 4.89487265e+00, 8.65150990e-02],

[-5.37913540e-02, 6.08999935e+00, 1.07312723e-01],

[ 4.17548207e-02, 6.81189745e+00, 1.46168807e-01],

[ 4.29923830e-02, 7.57912115e+00, 1.81007414e-01],

[ 6.39358198e-02, 9.28012949e+00, 1.58425867e-01],

[-6.26090674e-02, 1.09153417e+01, 1.42354643e-01],

[ 2.17990649e-02, 1.11140700e+01, 1.95319236e-01],

[-4.07478530e-02, 1.18101844e+01, 2.24222982e-01],

[-5.96051715e-02, 1.33034217e+01, 2.07198464e-01],

[ 1.16491739e-02, 1.33606016e+01, 2.70411346e-01],

[-5.09339524e-02, 1.44564831e+01, 2.72512353e-01]])

array([[ 3.15982571e-01, 4.10370250e+01, 1.49372521e-10],

[-5.88083875e-02, 4.24619648e+01, 6.01868337e-10],

[-1.74572953e-01, 5.50495642e+01, 6.70101585e-12],

[-8.21849192e-02, 5.78462709e+01, 8.21956756e-12],

[ 1.09130349e-01, 6.27897199e+01, 3.21823058e-12],

[ 1.49917833e-01, 7.21421520e+01, 1.48554920e-13],

[ 1.77317263e-02, 7.22733120e+01, 5.12360612e-13],

[-9.50309310e-02, 7.60500252e+01, 3.03874327e-13],

[-1.88881390e-01, 9.10071964e+01, 1.02210118e-15],

[-1.51868051e-01, 1.00700990e+02, 3.94492110e-17],

[ 3.62650860e-01, 1.56116450e+02, 8.36001979e-28],

[ 3.64378402e-01, 2.12202401e+02, 9.79513166e-39]])可以看到残差序列都是相关的,单纯的加法模型并不适合。

再次回到之前的自相关图,因为均不截尾,所以构建ARMA(1,1)模型

在考虑季节自相关特征,考虑季节效应周期(这里是一年,12阶延迟)倍数的相关系数,也就是12,24等

plot_acf(dx12,lags=[i for i in range(12,48,12)]).show()

plot_pacf(dx12,lags=[i for i in range(12,48,12)]).show()

可以看到自相关系数延迟12阶显著非0,但是延迟24阶落入两倍标准差内。而偏相关系数延迟12阶和24阶都显著非0,认为自相关1阶截尾,偏自相关拖尾,所以是\(ARIMA(1,1,1)\times(0,1,1)_{12}\)

array([[ 4.21220154e-02, 7.29235657e-01, 3.93131054e-01],

[ 3.45447505e-02, 1.22091516e+00, 5.43102298e-01],

[ 5.26569785e-03, 1.23236768e+00, 7.45252129e-01],

[-5.54856194e-03, 1.24511513e+00, 8.70616308e-01],

[ 8.40985550e-02, 4.18084466e+00, 5.23683554e-01],

[ 4.87304329e-02, 5.16898472e+00, 5.22329615e-01],

[-4.78427525e-02, 6.12382771e+00, 5.25367445e-01],

[ 1.45962355e-02, 6.21292525e+00, 6.23394560e-01],

[-3.75830490e-02, 6.80510717e+00, 6.57402303e-01],

[-6.54153133e-02, 8.60364592e+00, 5.70085780e-01],

[ 2.80827570e-02, 8.93594796e+00, 6.27804691e-01],

[-4.38198976e-02, 9.74707998e+00, 6.38138285e-01]])显著性检验通过,系数检验也通过

fig,axes=plt.subplots(figsize=(12,4))

axes.plot(data,label='raw')

axes.plot(mod.predict(0,480),label='predict')

plt.legend()[<matplotlib.lines.Line2D at 0x168deed5f08>]

[<matplotlib.lines.Line2D at 0x168deeb15c8>]

<matplotlib.legend.Legend at 0x168db920f88>

11.2.7.5 指数平滑模型

- Holt线性趋势模型

Holt 在1957年把简单的指数平滑模型进行了延伸,能够预测包含趋势的数据,该方法包含一个预测方程和两个平滑方程(一个用于水平,另一个用于趋势)

\[\begin{align*} \text{Forecast equation}&& \hat{y}_{t+h|t} &= \ell_{t} + hb_{t} \\ \text{Level equation}&& \ell_{t} &= \alpha y_{t} + (1 - \alpha)(\ell_{t-1} + b_{t-1})\\ \text{Trend equation}&& b_{t} &= \beta^*(\ell_{t} - \ell_{t-1}) + (1 -\beta^*)b_{t-1} \end{align*}\]

其中 ltlt代表时刻t的预估水平, btbt代表时刻t的预测趋势(或坡度), αα是水平的平滑参数, β∗β∗是趋势的平滑参数。 这时候,预测函数不再是平的,而是具有趋势的。

- 指数趋势模型

另外一种Holt 线性模型的变体是指数趋势模型,这时水平和趋势不是相加的,而是相乘

\[\begin{align*} \hat {y}_{t+h|t} &= \ell_{t} b_{t}^h\\ \ell_{t} &= \alpha y_{t} + (1 - \alpha)(\ell_{t-1} b_{t-1})\\ b_{t} &= \beta^*\frac{\ell_{t}}{ \ell_{t-1}} + (1 -\beta^*)b_{t-1} \end{align*}\]

其中 btbt代表预估的增长率(以相对的形式而不是绝对的形式)。这时候的趋势不是线性的,而是指数的。

- 阻尼趋势模型

经验表明,Holt的线性模型和指数模型倾向于对未来预测值过高,特别是对于长期预测。Gardner 和 McKenzie (1985)引入了一种阻尼效应,倾向于在未来保持一个水平的线。包含阻尼的趋势被证明是一种非常有效的预测方法。

除了Holt的方法中的α和\(\beta^*\),该方法还包含阻尼参数0<ϕ<1:

\[\begin{align*} \hat {y}_{t+h|t} &= \ell_{t} + (\phi+\phi^2 + \dots + \phi^{h}) b_{t} \\ \ell_{t} &= \alpha y_{t} + (1 - \alpha)(\ell_{t-1} + \phi b_{t-1})\\ b_{t} &= \beta^*(\ell_{t} - \ell_{t-1}) + (1 -\beta^*)\phi b_{t-1}. \end{align*}\]

如果 ϕ=1,这种方法与Holt的线性模型相同。对于在0到1的值, ϕ对趋势产生阻尼效应。实际上, 当 h→∞时对于任何的 0<ϕ<1预测值收敛于 lT+ϕbT/(1−ϕ)。 误差校正形式是:

\[\begin{align*} \ell_{t} &= \ell_{t-1} + \phi b_{t-1} + \alpha e_{t} \\ b_{t} &= \phi b_{t-1}+ \alpha \beta^*e_{t}. \end{align*}\]

- 乘法阻尼趋势

Taylor(2003)引入了一种阻尼参数,建立了乘法阻尼趋势模型:

\[\begin{align*} \hat {y}_{t+h|t} &= \ell_{t}b_{t}^{(\phi+\phi^2 + \dots + \phi^{h})} \\ \ell_{t} &= \alpha y_{t} + (1 - \alpha)\ell_{t-1} b^\phi_{t-1}\\ b_{t} &= \beta^*\frac{\ell_{t}}{ \ell_{t-1}} + (1 -\beta^*)b_{t-1}^{\phi}. \end{align*}\]

这种方法的预测结果不像加法阻尼那么保守,误差校正形式是:

\[\begin{align*} \ell_{t} &= \ell_{t-1} b^\phi_{t-1}+\alpha e_{t}\\ b_{t} &= b^\phi_{t-1}+ \alpha \beta^*\frac{e_{t}}{\ell_{t-1}}. \end{align*}\]

- holt三参数模型

三次指数平滑在二次指数平滑的基础上保留了季节性的信息,使得其可以预测带有季节性的时间序列。三次指数平滑添加了一个新的参数p来表示平滑后的趋势。

三次指数平滑有累加和累乘两种方法。

季节加法模型:

\(a_0截距,b为斜率,\epsilon_t随机波动,服从N(0,\sigma^2)分布,c_t为t时刻有时间效应造成的序列偏差\)

\[x_t=a_0+bt+c_t+\epsilon_t\]

假设每个季节的周期长度为m期,每一期的季节指数为\(S_1,S_2,\dots,S_m\),不放假设t时刻为季节周期的第j期,则\(c_t\)可以表示为:\(c_t=S_j+e_t e_t \sim N(0,\sigma^2_e)\),则模型可以写成如下递推公式:

\[x_t=a_0+b(t-1)+b+c_t+\epsilon_t=(x_{t-1}-c_{t-1}-\epsilon_{t-1})+b+\epsilon_t+(S_j+e_t)\]

不妨记:

\(a(t-1)=x_{t-1}-c_{t-1}-\epsilon_{t-1}\)

\(b(t)=b+\epsilon_t\)

\(c(t)=S_j+e_t\)

显然,\(a(t-1)\)是t-1时刻消除季节效应的序列截距项的无偏估计值,\(b(t)\)是t时刻斜率b的无偏估计值,c(t)是t时刻季节指数S_j的无偏估计值.

则:\(x_t=a(t-1)+b(t)+c(t)\)

Holt-Winters三参数指数模型就是分别使用指数平滑的方法,迭代递推参数\(\hat{a}(t),\hat{b}(t)和\hat{c}_t\)的值,递推公式如下:

\(\hat{a}(t)=\alpha[x_t-c(t-m)]+(1-\alpha)[\hat(a)(t-1)+\hat(b)(t-1)]\)

\(\hat{b}(t)=\beta[\hat{a}(t)-\hat{a}(t-1)]+(1-\beta)\hat{b}(t-1)\)

\(\hat{c}(t)=\gamma[x_t-\hat{a}(t)]+(1-\gamma)c(t-m)\)

式中,\(x_t\)为序列在t时刻得到的最新观察值;m是季节效应的周期长度;\(\alpha,\beta,\gamma\)均为平滑系数,满足\(0<\alpha,\beta,\gamma<1\)

使用holt-Winters三参数指数平滑加法公式,向前k期的预测值为:

\(\hat{x}_{t+k}=\hat{a}(t)+\hat{b}(t)k+\hat{c}(t+k),\forall k \geq 1\)

假设t+k期为季节周期的第j期,则\(\hat{c}(t+k)=\hat{S}_k(j=1,2,3,\dots,m)\)

季节乘法模型

对于乘法模型,序列通常可以表达为如下模型结构:

\(x_t=(a_0+bt+\epsilon_t)c_t\)

式中,\(a_0\)为截距;b为斜率.\(\epsilon_t\)为随机波动且\(\epsilon_t\sim N(0,sigma^2)\);c_t为t时刻的季节效应;

假设每个季节的周期长度为m期,每一期的季节指数为\(S_1,S_2,\dots,S_m\),不放假设t时刻为季节周期的第j期,则\(c_t\)可以表示为:\(c_t=S_j+e_t e_t \sim N(0,\sigma^2_e)\),则模型可以写成如下递推公式:

\[x_t=[a_0+b(t-1)+b+\epsilon_t]c_t=[(x_{t-1}/c_{t-1}-\epsilon_{t-1})+b+\epsilon_t](S_j+e_t)\]

不妨记:

\(a(t-1)=x_{t-1}/c_{t-1}-\epsilon_{t-1}\)

\(b(t)=b+\epsilon_t\)

\(c(t)=S_j+e_t\)

显然,a(t-1)是t-1时刻消除季节效应的序列截距的无偏估计值,b(t)是t时刻序列斜率b的无偏估计值,c(t)是t时刻序列季节指数\(S_j\)的无偏估计值

则模型可以表示为:

\[x_t=[a(t-1)+b(t)]c(t)\]

式中三个参数的地推公式是:

\(\hat{a}(t)=\alpha[x_t/c(t-m)]+(1-\alpha)[\hat(a)(t-1)+\hat(b)(t-1)]\)

\(\hat{b}(t)=\beta[\hat{a}(t)-\hat{a}(t-1)]+(1-\beta)\hat{b}(t-1)\)

\(\hat{c}(t)=\gamma[x_t/\hat{a}(t)]+(1-\gamma)c(t-m)\)

式中,\(x_t\)为序列在t时刻得到的最新观察值;m是季节效应的周期长度;\(\alpha,\beta,\gamma\)均为平滑系数,满足\(0<\alpha,\beta,\gamma<1\)

使用holt-Winters三参数指数平滑加法公式,向前k期的预测值为:

\(\hat{x}_{t+k}=[\hat{a}(t)+\hat{b}(t)k]\hat{c}(t+k),\forall k \geq 1\)

假设t+k期为季节周期的第j期,则\(\hat{c}(t+k)=\hat{S}_k(j=1,2,3,\dots,m)\)

11.2.7.6 简单指数平滑模型

模型没有长期趋势和季节效应

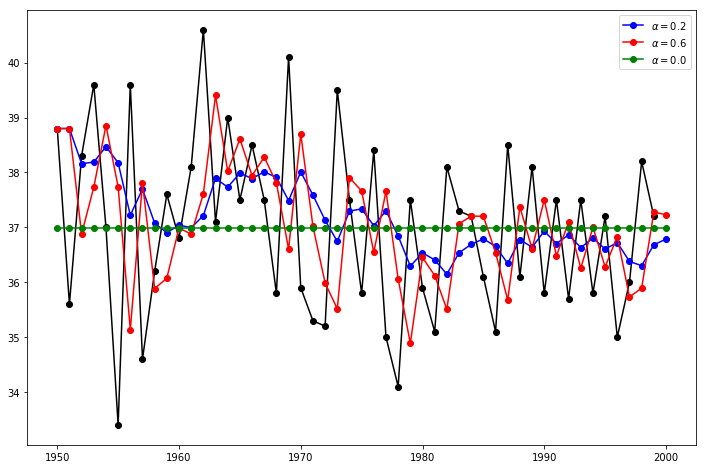

#Here we run three variants of simple exponential smoothing:

#In fit1 we do not use the auto optimization but instead choose to explicitly provide the model with the α=0.2 parameter

#In fit2 as above we choose an α=0.6

#In fit3 we allow statsmodels to automatically find an optimized α value for us. This is the recommended approach.

data=pd.read_excel('./习题与案例数据/案例数据/A1_18.xlsx')

data.index=pd.date_range('1949','1999',freq='a')

data.index

del data['year']

dataDatetimeIndex(['1949-12-31', '1950-12-31', '1951-12-31', '1952-12-31',

'1953-12-31', '1954-12-31', '1955-12-31', '1956-12-31',

'1957-12-31', '1958-12-31', '1959-12-31', '1960-12-31',

'1961-12-31', '1962-12-31', '1963-12-31', '1964-12-31',

'1965-12-31', '1966-12-31', '1967-12-31', '1968-12-31',

'1969-12-31', '1970-12-31', '1971-12-31', '1972-12-31',

'1973-12-31', '1974-12-31', '1975-12-31', '1976-12-31',

'1977-12-31', '1978-12-31', '1979-12-31', '1980-12-31',

'1981-12-31', '1982-12-31', '1983-12-31', '1984-12-31',

'1985-12-31', '1986-12-31', '1987-12-31', '1988-12-31',

'1989-12-31', '1990-12-31', '1991-12-31', '1992-12-31',

'1993-12-31', '1994-12-31', '1995-12-31', '1996-12-31',

'1997-12-31', '1998-12-31'],

dtype='datetime64[ns]', freq='A-DEC')| temp | |

|---|---|

| 1949-12-31 | 38.8 |

| 1950-12-31 | 35.6 |

| 1951-12-31 | 38.3 |

| 1952-12-31 | 39.6 |

| 1953-12-31 | 37.0 |

| 1954-12-31 | 33.4 |

| 1955-12-31 | 39.6 |

| 1956-12-31 | 34.6 |

| 1957-12-31 | 36.2 |

| 1958-12-31 | 37.6 |

| 1959-12-31 | 36.8 |

| 1960-12-31 | 38.1 |

| 1961-12-31 | 40.6 |

| 1962-12-31 | 37.1 |

| 1963-12-31 | 39.0 |

| 1964-12-31 | 37.5 |

| 1965-12-31 | 38.5 |

| 1966-12-31 | 37.5 |

| 1967-12-31 | 35.8 |

| 1968-12-31 | 40.1 |

| 1969-12-31 | 35.9 |

| 1970-12-31 | 35.3 |

| 1971-12-31 | 35.2 |

| 1972-12-31 | 39.5 |

| 1973-12-31 | 37.5 |

| 1974-12-31 | 35.8 |

| 1975-12-31 | 38.4 |

| 1976-12-31 | 35.0 |

| 1977-12-31 | 34.1 |

| 1978-12-31 | 37.5 |

| 1979-12-31 | 35.9 |

| 1980-12-31 | 35.1 |

| 1981-12-31 | 38.1 |

| 1982-12-31 | 37.3 |

| 1983-12-31 | 37.2 |

| 1984-12-31 | 36.1 |

| 1985-12-31 | 35.1 |

| 1986-12-31 | 38.5 |

| 1987-12-31 | 36.1 |

| 1988-12-31 | 38.1 |

| 1989-12-31 | 35.8 |

| 1990-12-31 | 37.5 |

| 1991-12-31 | 35.7 |

| 1992-12-31 | 37.5 |

| 1993-12-31 | 35.8 |

| 1994-12-31 | 37.2 |

| 1995-12-31 | 35.0 |

| 1996-12-31 | 36.0 |

| 1997-12-31 | 38.2 |

| 1998-12-31 | 37.2 |

fit1 = tsa.SimpleExpSmoothing(data).fit(smoothing_level=0.2,optimized=False)

fcast1 = fit1.predict(0,50)

fit2 = tsa.SimpleExpSmoothing(data).fit(smoothing_level=0.6,optimized=False)

fcast2 = fit2.predict(0,50)

fit3 = tsa.SimpleExpSmoothing(data).fit()

fcast3 = fit3.predict(0,50)

fig,ax=plt.subplots(figsize=(12,8))

ax.plot(data,marker='o', color='black')

ax.plot(fcast1,marker='o', color='blue', label=r'$\alpha=0.2$')

ax.plot(fcast2,marker='o', color='red', label=r'$\alpha=0.6$')

ax.plot(fcast3,marker='o', color='green', label=r'$\alpha=%s$'%fit3.model.params['smoothing_level'])

ax.legend()

plt.show()[<matplotlib.lines.Line2D at 0x168dbff8308>]

[<matplotlib.lines.Line2D at 0x168dbfdf188>]

[<matplotlib.lines.Line2D at 0x168dbfce788>]

[<matplotlib.lines.Line2D at 0x168dbfdf488>]

<matplotlib.legend.Legend at 0x168dbfce808>

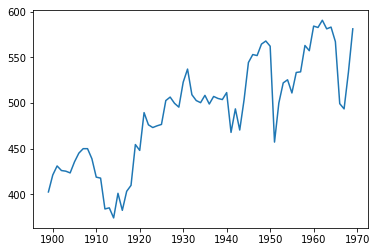

11.2.7.7 指数平滑-holt两参数

对于含有线性趋势的序列进行预测

data=pd.read_excel('./习题与案例数据/案例数据/A1_19.xlsx')

data.index=pd.date_range('1898','1969',freq='a')

del data['year']

data| water | |

|---|---|

| 1898-12-31 | 402.8 |

| 1899-12-31 | 421.3 |

| 1900-12-31 | 431.2 |

| 1901-12-31 | 426.2 |

| 1902-12-31 | 425.5 |

| … | … |

| 1964-12-31 | 567.1 |

| 1965-12-31 | 499.3 |

| 1966-12-31 | 493.6 |

| 1967-12-31 | 533.7 |

| 1968-12-31 | 581.1 |

71 rows × 1 columns

[<matplotlib.lines.Line2D at 0x168dcfc6d08>]

Holt's Method

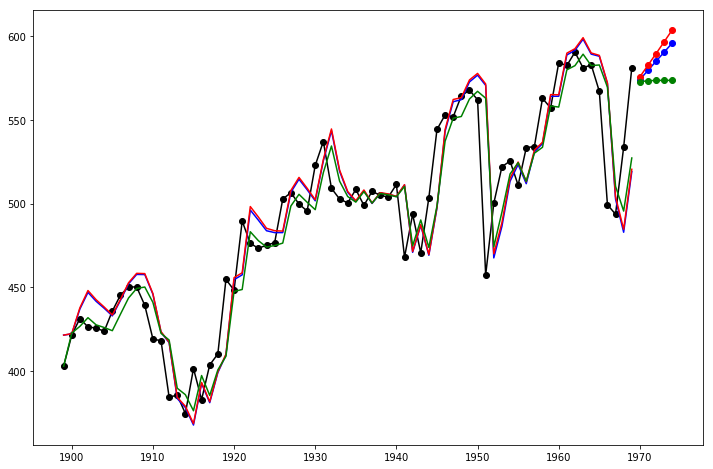

Lets take a look at another example. This time we use air pollution data and the Holt's Method. We will fit three examples again.

In fit1 we again choose not to use the optimizer and provide explicit values for α=0.8 and β=0.2

In fit2 we do the same as in fit1 but choose to use an exponential model rather than a Holt's additive model.

In fit3 we used a damped versions of the Holt's additive model but allow the dampening parameter ϕ to be optimized while fixing the values for α=0.8 and β=0.2fit1 = tsa.Holt(data).fit(smoothing_level=0.8, smoothing_slope=0.2, optimized=False)

fcast1 = fit1.forecast(5)

fit2 = tsa.Holt(data, exponential=True).fit(smoothing_level=0.8, smoothing_slope=0.2, optimized=False)

fcast2 = fit2.forecast(5)

fit3 = tsa.Holt(data, damped=True).fit(smoothing_level=0.8, smoothing_slope=0.2)

fcast3 = fit3.forecast(5)

fig,ax=plt.subplots(figsize=(12,8))

ax.plot(data,color="black", marker="o")

ax.plot(fit1.fittedvalues, color='blue')

ax.plot(fcast1, color='blue', marker="o")

ax.plot(fit2.fittedvalues,color='red')

ax.plot(fcast2, color='red', marker="o")

ax.plot(fit3.fittedvalues, color='green')

ax.plot(fcast3, color='green', marker="o")

plt.show()[<matplotlib.lines.Line2D at 0x168dc001d48>]

[<matplotlib.lines.Line2D at 0x168dd00a088>]

[<matplotlib.lines.Line2D at 0x168dd00a288>]

[<matplotlib.lines.Line2D at 0x168dd011088>]

[<matplotlib.lines.Line2D at 0x168dd00aa48>]

[<matplotlib.lines.Line2D at 0x168dd011b48>]

[<matplotlib.lines.Line2D at 0x168dd011d88>]

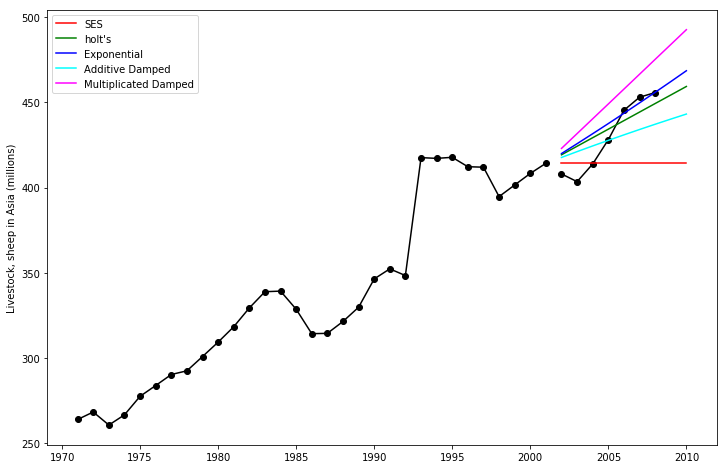

Seasonally adjusted data

Lets look at some seasonally adjusted livestock data. We fit five Holt’s models. The below table allows us to compare results when we use exponential versus additive and damped versus non-damped.

Note: fit4 does not allow the parameter ϕ to be optimized by providing a fixed value of ϕ=0.98

data = [263.9177, 268.3072, 260.6626, 266.6394, 277.5158, 283.834 , 290.309 , 292.4742, 300.8307, 309.2867, 318.3311, 329.3724, 338.884 , 339.2441, 328.6006, 314.2554, 314.4597, 321.4138, 329.7893, 346.3852, 352.2979, 348.3705, 417.5629, 417.1236, 417.7495, 412.2339, 411.9468, 394.6971, 401.4993, 408.2705, 414.2428]

index= pd.date_range(start='1970', end='2001', freq='A')

livestock2 = pd.Series(data, index)

data = [407.9979 , 403.4608, 413.8249, 428.105 , 445.3387, 452.9942, 455.7402]

index= pd.date_range(start='2001', end='2008', freq='A')

livestock3 = pd.Series(data, index)

fit1 = tsa.SimpleExpSmoothing(livestock2).fit()

fit2 = tsa.Holt(livestock2).fit()

fit3 = tsa.Holt(livestock2,exponential=True).fit()

fit4 = tsa.Holt(livestock2,damped=True).fit(damping_slope=0.98)

fit5 = tsa.Holt(livestock2,exponential=True,damped=True).fit()

params = ['smoothing_level', 'smoothing_slope', 'damping_slope', 'initial_level', 'initial_slope']

results=pd.DataFrame(np.zeros((6,5)),index=[r"$\alpha$",r"$\beta$",r"$\phi$",r"$l_0$","$b_0$","SSE"] ,columns=['SES', "Holt's","Exponential", "Additive", "Multiplicative"])

results["SES"] = [fit1.params[p] for p in params] + [fit1.sse]

results["Holt's"] = [fit2.params[p] for p in params] + [fit2.sse]

results["Exponential"] = [fit3.params[p] for p in params] + [fit3.sse]

results["Additive"] = [fit4.params[p] for p in params] + [fit4.sse]

results["Multiplicative"] = [fit5.params[p] for p in params] + [fit5.sse]

results| SES | Holt’s | Exponential | Additive | Multiplicative | |

|---|---|---|---|---|---|

| \(\alpha\) | 1.000000 | 0.974306 | 0.977633 | 0.978847 | 0.974911 |

| \(\beta\) | NaN | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| \(\phi\) | NaN | NaN | NaN | 0.980000 | 0.981646 |

| \(l_0\) | 263.917700 | 258.882647 | 260.341560 | 257.357648 | 258.951730 |

| \(b_0\) | NaN | 5.010775 | 1.013780 | 6.644538 | 1.038145 |

| SSE | 6761.350218 | 6004.138200 | 6104.194746 | 6036.555004 | 6081.995045 |

Plots of Seasonally Adjusted Data The following plots allow us to evaluate the level and slope/trend components of the above table’s fits.

for fit in [fit2,fit4]:

plt.plot(pd.DataFrame(np.c_[fit.level,fit.slope]).rename(columns={0:'level',1:'slope'}))

plt.show()

print('Figure 7.4: Level and slope components for Holt’s linear trend method and the additive damped trend method.')[<matplotlib.lines.Line2D at 0x168dec4d308>,

<matplotlib.lines.Line2D at 0x168dec4d4c8>]

[<matplotlib.lines.Line2D at 0x168deca9908>,

<matplotlib.lines.Line2D at 0x168deca9ac8>]

Figure 7.4: Level and slope components for Holt’s linear trend method and the additive damped trend method.Comparison¶

Here we plot a comparison Simple Exponential Smoothing and Holt’s Methods for various additive, exponential and damped combinations. All of the models parameters will be optimized by statsmodels.

fit1 = tsa.SimpleExpSmoothing(livestock2).fit()

fcast1 = fit1.forecast(9)

fit2 = tsa.Holt(livestock2).fit()

fcast2 = fit2.forecast(9)

fit3 = tsa.Holt(livestock2, exponential=True).fit()

fcast3 = fit3.forecast(9)

fit4 = tsa.Holt(livestock2, damped=True).fit(damping_slope=0.98)

fcast4 = fit4.forecast(9)

fit5 = tsa.Holt(livestock2, exponential=True, damped=True).fit()

fcast5 = fit5.forecast(9)

fig,ax=plt.subplots(figsize=(12,8))

ax .plot(livestock2,color="black", marker="o")

ax.plot(livestock3 ,color="black", marker="o")

ax.plot(fcast1, color='red',label='SES')

ax.plot(fcast2, color='green',label="holt's")

ax.plot( fcast3,color='blue',label="Exponential")

ax.plot( fcast4,color='cyan',label="Additive Damped")

ax.plot( fcast5,color='magenta',label='Multiplicated Damped')

ax.set_ylabel('Livestock, sheep in Asia (millions)')

plt.legend()

plt.show()

print('Figure 7.5: Forecasting livestock, sheep in Asia: comparing forecasting performance of non-seasonal methods.')[<matplotlib.lines.Line2D at 0x168e1383948>]

[<matplotlib.lines.Line2D at 0x168e13a88c8>]

[<matplotlib.lines.Line2D at 0x168e13afc08>]

[<matplotlib.lines.Line2D at 0x168e13afbc8>]

[<matplotlib.lines.Line2D at 0x168e13b2408>]

[<matplotlib.lines.Line2D at 0x168e13b2b48>]

[<matplotlib.lines.Line2D at 0x168e13b2308>]

Text(0, 0.5, 'Livestock, sheep in Asia (millions)')

<matplotlib.legend.Legend at 0x168e13b77c8>

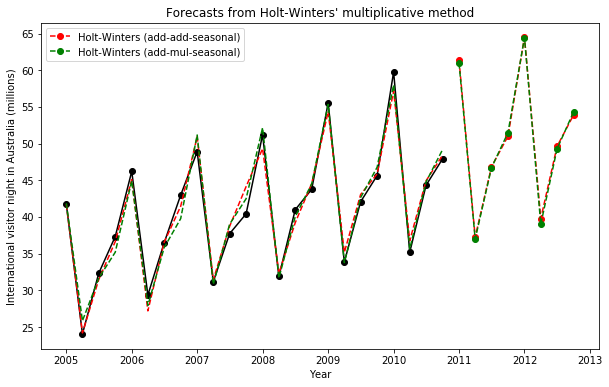

Figure 7.5: Forecasting livestock, sheep in Asia: comparing forecasting performance of non-seasonal methods.11.2.7.8 holt-winters三参数季节加法和乘法模型

tsa.ExponentialSmoothing(data,seasonal_periods,trend='add'或'mul',seasonal='add'或'mut')#seasonal选项决定了加法还是乘法模型

data = [41.7275, 24.0418, 32.3281, 37.3287, 46.2132, 29.3463, 36.4829, 42.9777, 48.9015, 31.1802, 37.7179, 40.4202, 51.2069, 31.8872, 40.9783, 43.7725, 55.5586, 33.8509, 42.0764, 45.6423, 59.7668, 35.1919, 44.3197, 47.9137]

index= pd.date_range(start='2005', end='2010-Q4', freq='QS-OCT')

aust = pd.Series(data, index)fit1 = tsa.ExponentialSmoothing(aust, seasonal_periods=4, trend='add', seasonal='add').fit(use_boxcox=True)

fit2 = tsa.ExponentialSmoothing(aust, seasonal_periods=4, trend='add', seasonal='mul').fit(use_boxcox=True)

fit3 = tsa.ExponentialSmoothing(aust, seasonal_periods=4, trend='add', seasonal='add', damped=True).fit(use_boxcox=True)

fit4 = tsa.ExponentialSmoothing(aust, seasonal_periods=4, trend='add', seasonal='mul', damped=True).fit(use_boxcox=True)

results=pd.DataFrame(np.zeros((7,4)),index=[r"$\alpha$",r"$\beta$",r"$\phi$",r"$\gamma$",r"$l_0$","$b_0$","SSE"],columns=["Additive","Multiplicative","Additive Dam","Multiplica Dam"])

params = ['smoothing_level', 'smoothing_slope', 'damping_slope', 'smoothing_seasonal', 'initial_level', 'initial_slope']

results["Additive"] = [fit1.params[p] for p in params] + [fit1.sse]

results["Multiplicative"] = [fit2.params[p] for p in params] + [fit2.sse]

results["Additive Dam"] = [fit3.params[p] for p in params] + [fit3.sse]

results["Multiplica Dam"] = [fit4.params[p] for p in params] + [fit4.sse]

fig,ax=plt.subplots(figsize=(10,6))

ax .plot(aust,marker='o', color='black' )

ax.set_ylabel("International visitor night in Australia (millions)")

ax.set_xlabel("Year")

ax.set_title("Forecasts from Holt-Winters' multiplicative method")

ax.plot(fit1.fittedvalues, ls='--', color='red')

ax.plot(fit2.fittedvalues, ls='--', color='green')

ax.plot(fit1.forecast(8), ls='--', marker='o', color='red', label='Holt-Winters (add-add-seasonal)')

ax.plot(fit2.forecast(8), ls='--', marker='o', color='green',label='Holt-Winters (add-mul-seasonal)')

plt.legend()

plt.show()

print("Figure 7.6: Forecasting international visitor nights in Australia using Holt-Winters method with both additive and multiplicative seasonality.")

results[<matplotlib.lines.Line2D at 0x168dd087b08>]

Text(0, 0.5, 'International visitor night in Australia (millions)')

Text(0.5, 0, 'Year')

Text(0.5, 1.0, "Forecasts from Holt-Winters' multiplicative method")

[<matplotlib.lines.Line2D at 0x168dec3f988>]

[<matplotlib.lines.Line2D at 0x168dec5c348>]

[<matplotlib.lines.Line2D at 0x168dc093a88>]

[<matplotlib.lines.Line2D at 0x168dececa88>]

<matplotlib.legend.Legend at 0x168dec08588>

Figure 7.6: Forecasting international visitor nights in Australia using Holt-Winters method with both additive and multiplicative seasonality.| Additive | Multiplicative | Additive Dam | Multiplica Dam | |

|---|---|---|---|---|

| \(\alpha\) | 4.546258e-01 | 3.659123e-01 | 3.231104e-08 | 0.000182 |

| \(\beta\) | 1.634586e-08 | 6.701126e-18 | 3.081400e-08 | 0.000182 |

| \(\phi\) | NaN | NaN | 9.453152e-01 | 0.913648 |

| \(\gamma\) | 5.244178e-01 | 9.705372e-12 | 7.167742e-06 | 0.000000 |

| \(l_0\) | 1.421751e+01 | 1.454863e+01 | 1.418138e+01 | 14.534854 |

| \(b_0\) | 1.307802e-01 | 1.661316e-01 | 2.380511e-01 | 0.484783 |

| SSE | 5.001656e+01 | 4.307003e+01 | 3.531783e+01 | 39.710958 |

The Internals It is possible to get at the internals of the Exponential Smoothing models.

Here we show some tables that allow you to view side by side the original values \(y_t\) , the level \(l_t\) , the trend \(b_t\) , the season \(s_t\) and the fitted values \(\hat{y}_t\) .

df = pd.DataFrame(np.c_[aust, fit1.level, fit1.slope, fit1.season, fit1.fittedvalues],

columns=[r'$y_t$',r'$l_t$',r'$b_t$',r'$s_t$',r'$\hat{y}_t$'],index=aust.index)

df.append(fit1.forecast(8).rename(r'$\hat{y}_t$').to_frame(), sort=True)| \(\hat{y}_t\) | \(b_t\) | \(l_t\) | \(s_t\) | \(y_t\) | |

|---|---|---|---|---|---|

| 2005-01-01 | 41.721215 | -34.969355 | 49.317641 | -7.593355 | 41.7275 |

| 2005-04-01 | 24.190230 | -35.452819 | 49.932455 | -25.834685 | 24.0418 |

| 2005-07-01 | 31.460507 | -36.532825 | 51.126190 | -19.183004 | 32.3281 |

| 2005-10-01 | 36.634747 | -37.397689 | 52.210159 | -15.209769 | 37.3287 |

| 2006-01-01 | 45.097771 | -38.467268 | 53.476787 | -7.837229 | 46.2132 |

| 2006-04-01 | 27.191784 | -40.276317 | 55.513864 | -27.017364 | 29.3463 |

| 2006-07-01 | 36.544233 | -40.625063 | 56.224501 | -19.713874 | 36.4829 |

| 2006-10-01 | 41.449470 | -42.041800 | 57.766129 | -15.523362 | 42.9777 |

| 2007-01-01 | 50.934532 | -41.543834 | 57.536773 | -7.588696 | 48.9015 |

| 2007-04-01 | 31.418265 | -42.197870 | 58.151045 | -26.874311 | 31.1802 |

| 2007-07-01 | 38.718351 | -42.303520 | 58.363042 | -20.191961 | 37.7179 |

| 2007-10-01 | 44.140653 | -41.085817 | 57.181928 | -14.982846 | 40.4202 |

| 2008-01-01 | 49.315801 | -42.961548 | 58.853067 | -8.619920 | 51.2069 |

| 2008-04-01 | 32.307035 | -43.186594 | 59.367061 | -27.309231 | 31.8872 |

| 2008-07-01 | 39.207484 | -44.827063 | 61.095687 | -20.925640 | 40.9783 |

| 2008-10-01 | 44.551298 | -44.899537 | 61.462251 | -17.319979 | 43.7725 |

| 2009-01-01 | 54.358133 | -46.192301 | 62.816914 | -7.881709 | 55.5586 |

| 2009-04-01 | 35.153884 | -45.980242 | 62.832235 | -28.447956 | 33.8509 |

| 2009-07-01 | 43.066515 | -46.228183 | 63.082736 | -20.550728 | 42.0764 |

| 2009-10-01 | 45.871197 | -46.852581 | 63.748943 | -17.997893 | 45.6423 |

| 2010-01-01 | 57.166649 | -48.770485 | 65.777689 | -7.372215 | 59.7668 |

| 2010-04-01 | 36.761415 | -48.308407 | 65.650109 | -29.816926 | 35.1919 |

| 2010-07-01 | 44.932523 | -48.798730 | 66.119529 | -21.517568 | 44.3197 |

| 2010-10-01 | 48.399603 | -49.269891 | 66.667513 | -18.522367 | 47.9137 |

| 2011-01-01 | 61.338004 | NaN | NaN | NaN | NaN |

| 2011-04-01 | 37.242913 | NaN | NaN | NaN | NaN |

| 2011-07-01 | 46.842710 | NaN | NaN | NaN | NaN |

| 2011-10-01 | 51.005356 | NaN | NaN | NaN | NaN |

| 2012-01-01 | 64.470967 | NaN | NaN | NaN | NaN |

| 2012-04-01 | 39.777051 | NaN | NaN | NaN | NaN |

| 2012-07-01 | 49.636039 | NaN | NaN | NaN | NaN |

| 2012-10-01 | 53.901669 | NaN | NaN | NaN | NaN |

df = pd.DataFrame(np.c_[aust, fit2.level, fit2.slope, fit2.season, fit2.fittedvalues],

columns=[r'$y_t$',r'$l_t$',r'$b_t$',r'$s_t$',r'$\hat{y}_t$'],index=aust.index)

df.append(fit2.forecast(8).rename(r'$\hat{y}_t$').to_frame(), sort=True)| \(\hat{y}_t\) | \(b_t\) | \(l_t\) | \(s_t\) | \(y_t\) | |

|---|---|---|---|---|---|

| 2005-01-01 | 41.860256 | -36.532222 | 51.246984 | 0.815871 | 41.7275 |

| 2005-04-01 | 25.838610 | -35.868807 | 50.738675 | 0.495361 | 24.0418 |

| 2005-07-01 | 31.659323 | -37.285903 | 52.062842 | 0.612972 | 32.3281 |

| 2005-10-01 | 35.189636 | -39.171170 | 54.189365 | 0.664165 | 37.3287 |

| 2006-01-01 | 44.929137 | -40.308071 | 55.708228 | 0.815030 | 46.2132 |

| 2006-04-01 | 27.933669 | -42.089577 | 57.758593 | 0.493042 | 29.3463 |

| 2006-07-01 | 35.824394 | -43.102570 | 59.129556 | 0.610078 | 36.4829 |

| 2006-10-01 | 39.768659 | -45.646232 | 61.909513 | 0.661689 | 42.9777 |

| 2007-01-01 | 51.174545 | -45.123562 | 61.858836 | 0.813571 | 48.9015 |

| 2007-04-01 | 30.814509 | -46.410933 | 63.137686 | 0.490286 | 31.1802 |

| 2007-07-01 | 39.009207 | -46.389041 | 63.329916 | 0.608210 | 37.7179 |

| 2007-10-01 | 42.486041 | -46.173405 | 63.146302 | 0.660426 | 40.4202 |

| 2008-01-01 | 52.174350 | -46.762004 | 63.704315 | 0.813364 | 51.2069 |

| 2008-04-01 | 31.677371 | -47.838278 | 64.873425 | 0.489542 | 31.8872 |

| 2008-07-01 | 40.035793 | -49.241989 | 66.470507 | 0.607660 | 40.9783 |

| 2008-10-01 | 44.515956 | -49.577850 | 67.068109 | 0.659565 | 43.7725 |

| 2009-01-01 | 55.343501 | -50.604967 | 68.192465 | 0.812746 | 55.5586 |

| 2009-04-01 | 33.773172 | -51.518074 | 69.287512 | 0.487867 | 33.8509 |

| 2009-07-01 | 42.644271 | -52.028198 | 69.973592 | 0.606360 | 42.0764 |

| 2009-10-01 | 46.778450 | -52.313589 | 70.368612 | 0.658677 | 45.6423 |

| 2010-01-01 | 58.009276 | -54.096698 | 72.214632 | 0.812268 | 59.7668 |

| 2010-04-01 | 35.648429 | -54.502798 | 72.912723 | 0.486508 | 35.1919 |

| 2010-07-01 | 44.784383 | -55.166772 | 73.686275 | 0.605385 | 44.3197 |

| 2010-10-01 | 49.174485 | -55.392542 | 74.032938 | 0.657808 | 47.9137 |

| 2011-01-01 | 60.967615 | NaN | NaN | NaN | NaN |

| 2011-04-01 | 36.993898 | NaN | NaN | NaN | NaN |

| 2011-07-01 | 46.712479 | NaN | NaN | NaN | NaN |

| 2011-10-01 | 51.482819 | NaN | NaN | NaN | NaN |

| 2012-01-01 | 64.456507 | NaN | NaN | NaN | NaN |

| 2012-04-01 | 39.017313 | NaN | NaN | NaN | NaN |

| 2012-07-01 | 49.291842 | NaN | NaN | NaN | NaN |

| 2012-10-01 | 54.320157 | NaN | NaN | NaN | NaN |

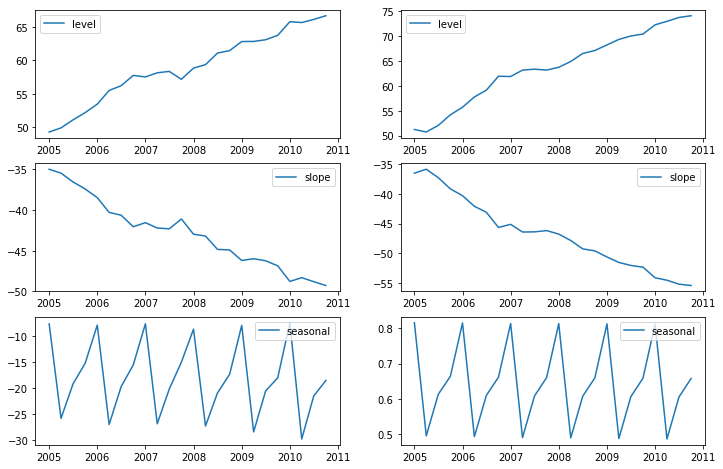

Finally lets look at the levels, slopes/trends and seasonal components of the models.

states1 = pd.DataFrame(np.c_[fit1.level, fit1.slope, fit1.season], columns=['level','slope','seasonal'], index=aust.index)

states2 = pd.DataFrame(np.c_[fit2.level, fit2.slope, fit2.season], columns=['level','slope','seasonal'], index=aust.index)

fig, [[ax1, ax4],[ax2, ax5], [ax3, ax6]] = plt.subplots(3, 2, figsize=(12,8))

ax1.plot(states1[['level']],label='level')

ax1.legend()

ax2.plot(states1[['slope']],label='slope')

ax2.legend()

ax3.plot(states1[['seasonal']],label='seasonal')

ax3.legend()

ax4.plot(states2[['level']],label='level')

ax4.legend()

ax5.plot(states2[['slope']],label='slope')

ax5.legend()

ax6.plot(states2[['seasonal']],label='seasonal')

ax6.legend()

plt.show()[<matplotlib.lines.Line2D at 0x168dbceab08>]

<matplotlib.legend.Legend at 0x168db928648>

[<matplotlib.lines.Line2D at 0x168dcf41bc8>]

<matplotlib.legend.Legend at 0x168db9ab9c8>

[<matplotlib.lines.Line2D at 0x168dc101cc8>]

<matplotlib.legend.Legend at 0x168dba4f3c8>

[<matplotlib.lines.Line2D at 0x168dcf46c08>]

<matplotlib.legend.Legend at 0x168dc0f6fc8>

[<matplotlib.lines.Line2D at 0x168dcf6cdc8>]

<matplotlib.legend.Legend at 0x168dc12e708>

[<matplotlib.lines.Line2D at 0x168db9ef548>]

<matplotlib.legend.Legend at 0x168db9c3208>

11.2.8 examples参考

ARMA模型,讲了平稳性检验,随机性检验,相关图绘制,模型定阶和构建,假设的检验,预测

ARIMA模型,讲了只有趋势项的情形,以及疏系数构建,以及ARIMA加法和乘法模型

指数平滑的例子,包括简单指数平滑,holt两参数平滑(无季节效应),holt三参数季节加法和乘法模型

ARIMA Example 4: ARMAX (Friedman)

This model demonstrates the use of explanatory variables (the X part of ARMAX). When exogenous regressors are included, the SARIMAX module uses the concept of “regression with SARIMA errors” (see http://robjhyndman.com/hyndsight/arimax/ for details of regression with ARIMA errors versus alternative specifications), so that the model is specified as:

\[y_t = \beta_t x_t + u_t \\ \phi_p (L) \tilde \phi_P (L^s) \Delta^d \Delta_s^D u_t = A(t) + \theta_q (L) \tilde \theta_Q (L^s) \epsilon_t\]

Notice that the first equation is just a linear regression, and the second equation just describes the process followed by the error component as SARIMA (as was described in example 3). One reason for this specification is that the estimated parameters have their natural interpretations.

This specification nests many simpler specifications. For example, regression with AR(2) errors is:

\[y_t = \beta_t x_t + u_t \\ (1 - \phi_1 L - \phi_2 L^2) u_t = A(t) + \epsilon_t\]

The model considered in this example is regression with ARMA(1,1) errors. The process is then written:

\[\text{consump}_t = \beta_0 + \beta_1 \text{m2}_t + u_t \\ (1 - \phi_1 L) u_t = (1 - \theta_1 L) \epsilon_t\]

Notice that β0 is, as described in example 1 above, not the same thing as an intercept specified by trend=‘c’. Whereas in the examples above we estimated the intercept of the model via the trend polynomial, here, we demonstrate how to estimate β0 itself by adding a constant to the exogenous dataset. In the output, the beta0 is called const, whereas above the intercept c was called intercept in the output.

# Dataset

friedman2 = requests.get('https://www.stata-press.com/data/r12/friedman2.dta').content

data = pd.read_stata(BytesIO(friedman2))

data.index = data.time

# Variables

endog = data.loc['1959':'1981', 'consump']

exog = sm.add_constant(data.loc['1959':'1981', 'm2'])

# Fit the model

mod = sm.tsa.statespace.SARIMAX(endog, exog, order=(1,0,1))

res = mod.fit(disp=False)

print(res.summary()) Statespace Model Results

==============================================================================

Dep. Variable: consump No. Observations: 92

Model: SARIMAX(1, 0, 1) Log Likelihood -340.508

Date: Sat, 10 Apr 2021 AIC 691.015

Time: 21:25:14 BIC 703.624

Sample: 01-01-1959 HQIC 696.105

- 10-01-1981

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -36.0620 56.639 -0.637 0.524 -147.073 74.949

m2 1.1220 0.036 30.826 0.000 1.051 1.193

ar.L1 0.9348 0.041 22.717 0.000 0.854 1.015

ma.L1 0.3091 0.089 3.488 0.000 0.135 0.483

sigma2 93.2558 10.889 8.565 0.000 71.915 114.597

===================================================================================

Ljung-Box (Q): 38.72 Jarque-Bera (JB): 23.49

Prob(Q): 0.53 Prob(JB): 0.00

Heteroskedasticity (H): 22.51 Skew: 0.17

Prob(H) (two-sided): 0.00 Kurtosis: 5.45

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

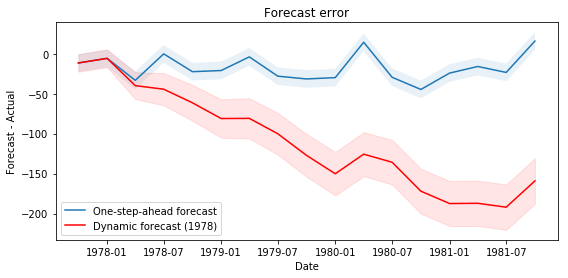

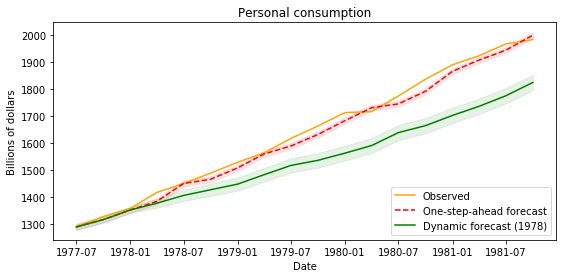

ARIMA Postestimation: Example 1 - Dynamic Forecasting

Here we describe some of the post-estimation capabilities of Statsmodels' SARIMAX.

First, using the model from example, we estimate the parameters using data that excludes the last few observations (this is a little artificial as an example, but it allows considering performance of out-of-sample forecasting and facilitates comparison to Stata's documentation).# Dataset

raw = pd.read_stata(BytesIO(friedman2))

raw.index = raw.time

data = raw.loc[:'1981']

# Variables

endog = data.loc['1959':, 'consump']

exog = sm.add_constant(data.loc['1959':, 'm2'])

nobs = endog.shape[0]